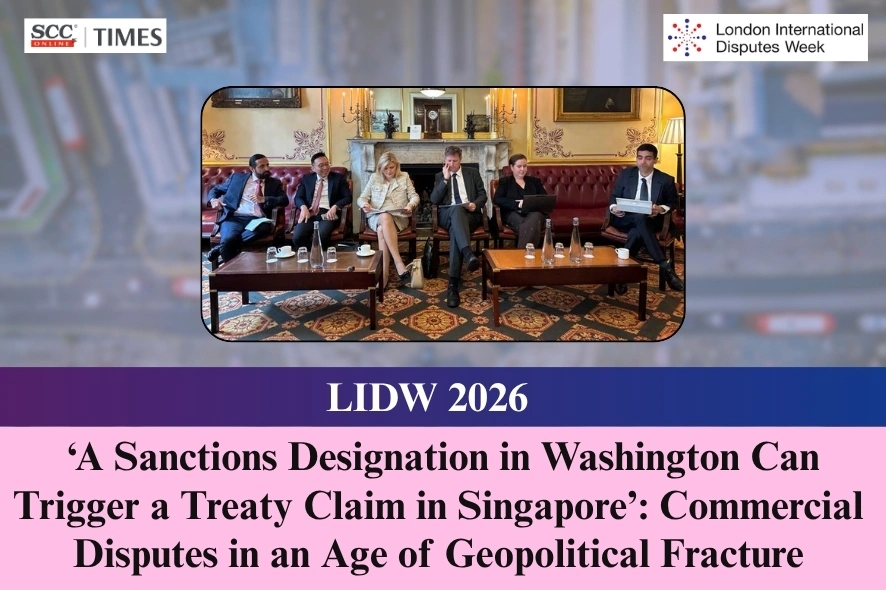

A panel of leading international arbitration practitioners and forensic quantum experts gathered at the City of London Club on 4 June 2026 under the auspices of London International Disputes Week (LIDW) 2026 to examine a question that has moved rapidly from academic conjecture to daily courtroom reality: how does the global “polycrisis”, the simultaneous collision of trade-policy weaponisation, kinetic conflicts, sanctions escalation and resource nationalism, translate into contractual stress, and what tools does commercial law offer parties caught in its wake?

The session, titled Under Fire: Commercial Disputes in an Age of Geopolitical Fracture, was co-moderated by Mr. Raunak Dhillon, Partner at Cyril Amarchand Mangaldas, and Mr. Montek Mayal, Partner and Head of Asia and Middle East at Osborne Partners. The panel comprised Mr. Nick Storrs, Partner at Taylor Wessing; Ms. Rebecca James, Partner at Linklaters; Mr. Paul Tan of One Essex Court; and Ms. Sylvia Tonova, Partner at Pinsent Masons. Discussion was structured around four themes: supply chain and contractual performance; investment and shareholder disputes; the state as a commercial actor; and quantum.

The Polycrisis Arrives in the Hearing Room

Opening the discussion, Mr. Raunak Dhillon described the term “polycrisis,” coined initially to capture the convergence of climate stress, energy insecurity and post-pandemic fragility as having migrated directly into commercial practice. He observed that a sanctions designation in Washington D.C. could now simultaneously trigger a force majeure notice in Singapore, a material adverse change dispute in London and a DCF valuation fight in a treaty arbitration, all against a background of kinetic conflict. Mr. Dhillon emphasised that these are not hypothetical chains of events and that these are the kinds of matters this panel has collectively worked on.

Asked to identify which category of dispute had grown most visibly in recent years, panellists pointed to overlapping fronts. Mr. Montek Mayal highlighted technology supply disputes, attributing their rise both to surging demand for memory chips and to the United States’ reshaping of global tech supply chains. He mentioned that it is something we are seeing an increase in and is going to continue to increase for the foreseeable future.

Mr. Nick Storrs described a matter arising directly from the Russia-Ukraine conflict, in which sanctions had made it impossible for a European client to exit a Russian counterparty relationship on commercially clean terms, producing not only a commercial arbitration seated in Asia but parallel proceedings in the Russian courts, anti-suit injunctions and, on top, a potential bilateral investment treaty (BIT) claim arising out of the Russian court’s conduct. He noted that the complexity of the matter kept increasing with time.

Ms. Rebecca James pointed to resource nationalism, including export bans and local content requirements applied to critical minerals essential to technology supply chains, as a trend generating both contract disputes and potential investment treaty claims.

Mr. Paul Tan identified a matter in which a United States executive order had impaired a counterparty’s ability to perform, producing a direct loss dispute, while also noting a rise in secondary disputes among Russian-linked vessel and cargo owners arising from the spike in oil import values to sanction-free jurisdictions such as Singapore. Mr. Dhillon, speaking from an Indian vantage point, drew attention to the knock-on effects of supply chain disruption on power purchase agreements and infrastructure projects, with import availability, pricing and timeline disputes all multiplying.

Force Majeure: The Contractual Battlefield

Turning to the legal mechanisms most contested when geopolitical disruption affects contractual performance, Ms. Rebecca James offered a systematic analysis of force majeure under common law. She reminded the audience that force majeure is not a free-standing common law doctrine but a purely contractual device, one whose effectiveness depends entirely on what the parties have agreed. The battleground, she said, lay in three questions: whether a defined force majeure event has occurred when properly construed; whether that event has met the contractual threshold for effect on performance, typically prevention (near-impossibility), material hindrance, or delay; and whether secondary conditions such as notice and mitigation efforts have been satisfied.

Ms. James noted that these clauses do not cater to a situation where things get harder or expensive. She briefly addressed the relationship between force majeure clauses and the common law doctrine of frustration, observing that where parties have allocated risks contractually, frustration has very little room to operate in practice, though creative attempts continue. She cited a recent case in which an early dismissal application succeeded under the arbitral rules after a frustration argument based on pandemic measures was advanced in the face of detailed contractual risk allocation.

Mr. Paul Tan, building on that analysis, identified three additional layers of difficulty. First, the definitional question: polycentric crises lead parties to re-characterise events. For example, arguing that hostilities in Ukraine or the Strait of Hormuz constitute a “conflict” rather than a “war,” so as to fall outside a standard force majeure clause. Second, the causation question: courts draw fine lines on what constitutes the effective cause of non-performance. He referred to a decision from Michigan in which a court held that the effective cause of one party’s inability to perform was a fall in the price of solar panels caused by Chinese dumping, not any governmental act even though the trade dispute was its ultimate origin. Third, the threshold question: high threshold set in common law jurisdictions. Adding to this, Mr. Tan said that he could not identify a decided case in which these doctrines had been successfully invoked in the context of a pure geopolitical event. The closest, he suggested, was a Singapore Court of Appeal decision on a sand ban, upheld only because the parties had contractually contemplated Indonesia as the sole source of supply.

Mr. Tan counselled that even where 100 per cent economic impact could be demonstrated, a figure he noted has not moved many Contracts for the International Sale of Goods (CISG) tribunals under Article 791, the courts would likely ask whether supply could have been obtained elsewhere.

“The moment the other side can point to an alternative source, even if the consequences on performance are astronomical, that in itself will not enable you to be a successful party invoking those defences.” Mr. Paul Tan

Ms. James and Mr. Tan both concluded with a drafting recommendation, parties must now assume volatility rather than stability, define qualifying events more precisely, consider quantitative or qualitative thresholds, or both, and critically build in middle-ground remedies such as price renegotiation or adjustment, rather than relying on all-or-nothing termination triggers. Mr. Tan observed that Courts and tribunals are very hesitant to discharge contracts, because the consequence is that performance is at an end. He further explained that if a contract allows for some middle ground, then a situation arises where parties are more prepared to accept.

Speaking from an Indian law perspective, Mr. Raunak Dhillon noted that the doctrine of frustration in India is codified under the Contract Act on the basis of impossibility, and that the Supreme Court has recently confirmed it must be true impossibility rather than mere onerousness, rejecting a claim by a private power developer whose coal import costs had risen sharply following Indonesia’s change to its coal regime.

Investment and Shareholder Disputes: MAC Clauses under Scrutiny

The second block addressed investment and shareholder disputes. Mr. Nick Storrs drew attention to a development in English contract law, an increasing judicial willingness to give effect to price renegotiation clauses that would formerly have been dismissed as unenforceable agreements to agree. A recent Court of Appeal decision had shown that English courts are prepared to look behind commercially sophisticated renegotiation mechanisms, particularly those containing a good faith obligation and imply a duty to agree on a reasonable price.

“Whether it’s your agreement to agree a reasonable price in the circumstances of some degree of uncertainty, the courts have an appetite to look at that and give it real meaning,” Mr. Storrs said, describing this as a development likely to continue as pricing uncertainty becomes the commercial norm.

Ms. Rebecca James added that the critical drafting step, for parties wishing to benefit from that trend, was to embed objective criteria such as a reasonable price standard or specific parameters in the renegotiation clause, so that a tribunal could give effect to it without overstepping its jurisdictional mandate.

Ms. Sylvia Tonova introduced a particular difficulty arising in public-private partnerships involving state-owned entities, where geopolitical stress can cause funding disagreements within a joint venture to escalate rapidly into a scenario in which the state actor pursues its position through sovereign rather than contractual means, turning a commercial dispute into a potential investment treaty claim. She explained that it is just an example of how geopolitical events put a strain on the contractual and commercial relationship, which then escalates to a sovereign interference.

On Material Adverse Change (MAC) and Material Adverse Effect (MAE) clauses, Mr. Paul Tan cautioned against treating them as reliable tools in geopolitical scenarios. Most such clauses carve out industry-wide or market-wide events, they are designed to address idiosyncratic deterioration of a specific company’s value, not macro shocks. Even where a clause could arguably be invoked, the burden of proving materiality remains heavy, English courts have indicated a threshold in the region of a 20 per cent drop in equity value, and the durational dimension adds further complexity.

“You could have a strike one day and then a certain leader of the free world says we are now in indefinite ceasefire. How do you predict it? It’s difficult. Perhaps that’s the role of the expert.” Mr. Paul Tan

Mr. Montek Mayal noted that the correlation between stock market movements and underlying geopolitical events has itself become unstable, a point with implications for the causation analysis in any MAC dispute.

Ms. James observed that in most contested MAC cases, the real battle is over cause, one party attributes deterioration to a volatile market and the other asserts that company-specific factors are the true driver.

“The real battle you’re having is what has, in fact, caused it, which can be incredibly complicated when you’ve got all of these different overlapping factors,” Ms. Rebecca James

The State as a Commercial Actor: Investment Treaty Protection

Ms. Sylvia Tonova addressed the central question of when sovereign action crosses the line from legitimate regulation into conduct triggering investment treaty protection. She cautioned against over-reliance on broad generalisations, urging that analysis must begin with the treaty text itself, noting the material differences between older-generation treaties, which were drafted in general terms and have sometimes been interpreted generously towards investors, and newer-generation treaties, which contain detailed carve-outs and qualifying conditions.

As a working principle, Ms. Tonova suggested that it is easier to impugn a government measure targeting a particular investor than a legislative measure of general application. She cited the Spanish renewable energy cases, where numerous tribunals found that Spain had radically altered the fundamental basis on which investors had invested, breaching the fair and equitable treatment (FET) standard. By contrast, broadly applicable legislative measures, as seen in the Argentine cases, supply the state with substantially more defensive arguments. Measures by the executive are more susceptible to challenge than legislative acts. She further expressed that judicial conduct is hardest of all to impugn, given that tribunals are not intended to act as courts of appeal over national court decisions.

Ms. Tonova drew attention to two emerging categories of cases.

-

sanctions-based treaty claims: she noted that proceedings have been brought by Russian individuals challenging the EU and possibly UK sanctions that resulted in their designation on sanctions lists and asset freezes. These cases, she said, are fascinating to monitor because, while they involve measures directed at a specific individual (which ordinarily makes them easier to challenge), they represent state action taken in direct response to a geopolitical event and engage a significant measure of deference towards state foreign policy.

-

Huawei v Sweden case2 brought under the China-Sweden BIT, concerning exclusion from Sweden’s 5G network — a case in which national security considerations are central but, she noted, the treaty in question apparently contains no essential security exception, leaving Sweden to advance arguments such as the police powers doctrine.

In response to a question from Mr. Raunak Dhillon on whether investor expectations are evolving in line with the changed geopolitical landscape, Ms. Tonova described the recently filed claim by a Singapore investor who had acquired an interest in a UK coal mine and was denied a planning consent following the UK Supreme Court’s Finch decision which required authorities to take into account scope 3 (downstream) greenhouse gas emissions when determining such applications. The investor has now commenced treaty proceedings under the 1975 UK-Singapore BIT, with Juan Fernandez-Armesto as presiding arbitrator. She questioned the investors’ legitimate expectations. She mentioned that they invested in 2022, before the ICJ climate opinion, but still at a time when climate change and net zero were very much part of UK government policy. She expressed that the investor would be hard-pressed to argue that this was not part of the landscape they should have taken into account.

Ms. Tonova also cautioned that many investors who come for advice after a geopolitical event materialises discover that they lack a BIT with the relevant state, a structural gap that is particularly acute for Chinese investors in the United States and Indian investors in China, where no applicable investment treaty exists. She mentioned that then the parties need to consider structuring.

Quantum: The Art of Valuation in Distorted Markets

The final block addressed the quantum dimension. Mr. Raunak Dhillon posed the valuation date question which is widely regarded as one of the most consequential choices in any damages analysis, to Mr. Nick Storrs and Ms. Sylvia Tonova. Mr. Storrs confirmed that the default starting point in most tribunals and courts is the date of breach, from which it requires something quite dramatic to move. In supply contract contexts, he explained, the existence of an available market for a substitute product will ordinarily produce a straightforward mitigation analysis, reducing the dispute to one of additional cost rather than the full value of the contract.

“The real exception is when you’re dealing with something which is truly unique that’s when you escape that argument and start to look at a different date.” Mr. Nick Stross

Ms. Tonova, noting that the question was “almost an art form”, observed that the difficulty is most acute in cases of continuing breach and where composite state responsibility is engaged. She confirmed that the date of breach remains the baseline, but flagged that investors sometimes argue for date of award in order to capture commodity or market price increases that have occurred since the state’s unlawful act and that the legal framework matters in lawful expropriation, the standard is clear i.e. fair market value at the day before expropriation, but in unlawful expropriation or FET breaches, the full reparation principle from the Chorzów Factory case3 applies, bringing a degree of flexibility that she acknowledged “gets into art.”

She also noted a recurring defensive argument by states at date of award that the particular investor would not, in fact, have survived to realise the upside, it would have become insolvent, or failed to obtain financing regardless of the state’s conduct, introducing causation and counterfactual questions into the valuation exercise.

Mr. Montek Mayal offered a perspective from quantum practice. Documentation is, in his view, the single most underestimated factor. In many disputes including, he noted, those involving private equity funds, the key forensic question is what was known, what was expected, and how risk was priced at the relevant time. Poor or absent documentation makes that analysis almost impossible. He also emphasised the increasing importance of rigorous causation analysis:

“To take damages, you still have to link the breach with the harm. In today’s world, with so many different factors at play, that linking has become even more important.” Mr. Montek Mayal

Closing Observations: Future-Proofing for a Volatile World

In their closing observations, panellists offered practical recommendations for commercial parties and counsel. Ms. James urged parties to draft contracts on an assumption of volatility rather than stability, invest in anticipating where political risks will crystallise for a given contract, and build in better exit routes. Mr. Storrs recommended greater clarity in price adjustment language, describing it as the most economically efficient resolution mechanism in long-term critical supply arrangements. Ms. Tonova advised that transactional mandates should routinely involve disputes lawyers at the negotiating stage, a point Mr. Tan echoed, observing that transactional lawyers tend to operate on the basis of the best-case scenario while disputes lawyers plan for the worst. Choice of seat, he added, is itself a variable that may need to be revisited, since geopolitical shifts can affect a seat’s perceived neutrality.

Mr. Dhillon, speaking from an Indian transactional and disputes perspective, called for stronger in-built contractual protective mechanisms, noting that the time had passed for treating force majeure and related clauses as mere theoretical escape hatches. He suggested that rather than look clauses just as clauses that one may not foresee using, one should have a strong in-built mechanisms for protection from situations as and when they arise. He endorsed the view that disputes lawyers should be brought into transactional negotiations at a deeper and earlier stage.

As geopolitical tensions continue to reshape global trade and investment flows, the panel made clear that businesses can no longer contract on the assumption of stability. Effective risk allocation, thoughtful drafting and strategic dispute planning are increasingly essential in a world where sanctions, conflicts and regulatory interventions can quickly transform commercial disagreements into complex, multi-jurisdictional disputes.

This report forms part of SCC Times’ special coverage of London International Disputes Week (LIDW) 2026. As a Media Partner for the event, SCC Times is reporting key conversations across the conference, highlighting emerging trends and perspectives from the international dispute resolution community.

SCC Times extends its appreciation to Zehra Naqvi, EBC—SCC Online Foreign Student Ambassador and Lawyer, for her on ground presence, valuable assistance and contribution to the reporting of this event.

Read more LIDW 2026 Coverage:

1. United Nations Convention on Contracts for the International Sale of Goods, Article 79

2. Huawei Technologies Co., Ltd. v. Kingdom of Sweden, ICSID (Case No. ARB/22/2)

3. Factory at Chorzów (Germany v. Poland), Merits, Judgment No. 13, 1928 PCIJ (Ser. A) No. 17.