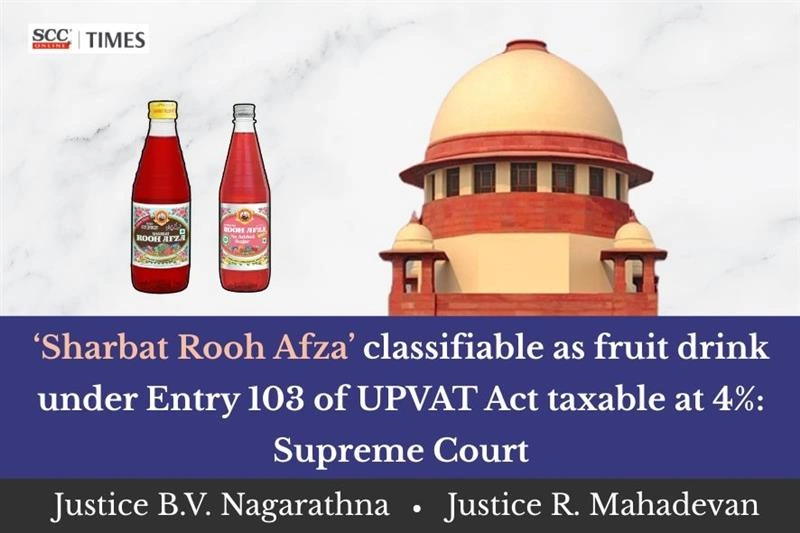

Supreme Court: While settling the controversy concerning the proper classification of “Sharbat Rooh Afza” under the Uttar Pradesh Value Added Tax Act, 2008 (UPVAT Act), and whether the said product is exigible to tax at the rate of 4% under Entry 103 of Part A of Schedule II or at the higher rate of 12.5% as an unclassified commodity under the residuary entry contained in Schedule V, a Division Bench of B.V. Nagarathna and R. Mahadevan,* JJ., allowed the appeal and held that ‘Sharbat Rooh Afza’ was classifiable under Entry 103 of Schedule II, Part A of the UPVAT Act as a fruit drink / processed fruit product and was exigible to VAT at the concessional rate of 4% during the relevant assessment years. The Court directed the respondent authorities to grant consequential relief, including refund or adjustment of excess tax paid, in accordance with law.

The appellant, M/s Hamdard (Wakf) Laboratories, is the manufacturer of “Sharbat Rooh Afza”, “a non-alcoholic sweetened beverage prepared from invert sugar and blended with fruit juices, vegetable extracts and added flavours”.

During the assessment period from 01 January 2008 to 31 March 2012, the appellant treated the product as a “fruit drink” or “processed fruit” falling under Entry 103 of Schedule II, Part A of the UPVAT Act, and paid VAT at 4%. Entry 103 covered “Processed or preserved vegetables and fruits including fruit jams, jelly, pickle, fruit squash, paste, fruit drink & fruit juice (whether in sealed containers or otherwise).”

The composition of the product disclosed 80% invert sugar syrup, 8% pineapple juice, 2% orange juice, and other distillates and extracts. The product thus admittedly contained 10% fruit juice.

The Assessing Authority, however, held that “Sharbat Rooh Afza” was an unclassified commodity taxable under Entry 1 of Schedule V, which applied to “All goods except goods mentioned or described in Schedule-I, Schedule-II, Schedule-III and Schedule-IV of this Act” at 12.5%.

The first appeals and second appeals before the Tribunal were dismissed. The Allahabad High Court affirmed the concurrent findings and held that “Sharbat Rooh Afza” did not qualify as a fruit drink under the residuary entry.

Aggrieved thereby, the appellant approached the Supreme Court.

The Court traced the evolution of the pre-VAT and post-VAT regime from the Uttar Pradesh Trade Tax Act, 1948 to the UPVAT Act and then to Uttar Pradesh Goods and Services Tax Act, 2017, and noted that the controversy was confined to classification under the UPVAT Act.

At the outset, the Court held that “a fiscal statute must be interpreted in its own language.” Regulatory enactments such as the Food Products Order, 1955 (FPO) operate in a distinct domain of quality control and safety and are “neither determinative nor conclusive for purposes of fiscal classification unless a taxing statute expressly incorporates or adopts such definitions.” Thus, It was held that the licensing norms under the FPO could not control the interpretation of an undefined fiscal entry.

The Court note that the expression “fruit drink” has not been defined under the UPVAT Act. It reiterated that in the absence of a statutory definition, classification must be determined by the common parlance test, i.e., “in commercial and popular sense by those who deal with it”

Relying on Ramavatar Budhaiprasad v. Asstt. STO, 1961 SCC OnLine SC 57, Indo International Industries v. CST, (1981) 2 SCC 528 and CCE v. Connaught Plaza Restaurant (P) Ltd., (2012) 13 SCC 639, the Court emphasised that word must be understood in its common parlance sense, commercial understanding must prevail over technical or dictionary meaning and marketing nomenclature is not decisive; and consumer perception must be established by objective material.

The Court found that the authorities relied primarily on licensing norms and the nomenclature “sharbat” rather than tangible evidence evidence of commercial perception. The Revenue had produced “no trade enquiry, consumer survey, market evidence or documentary material” to show that the product is not understood as a fruit-based beverage preparation. Accordingly, it was held that the Revenue had failed to discharge the burden cast upon it in law.

On the essential character test, the Court held that mechanical reliance on quantitative predominance of sugar syrup would be misplaced. It categorically observed that “classification must follow the component that confers upon the product its essential beverage character.”

The Court further emphasised that Entry 103 was couched in inclusive terms and did not prescribe any minimum threshold of fruit content. It would therefore be inappropriate “to read into the entry a rigid percentage requirement that the Legislature has consciously not provided”. Therefore, it was held that the expression “fruit drink” in Entry 103 cannot be confined solely to ready-to-consume bottled beverages and “fruit squashes, concentrates and sharbat preparations intended for dilution are all capable of being understood as fruit drink preparations.”

The Court reiterated that recourse to the residuary clause is permissible only when goods cannot reasonably be brought within a specific entry. It relied on Dunlop India Ltd. v. Union of India, (1976) 2 SCC 241, where this Court cautioned against consigning goods to the “orphanage of the residuary clause” where they bear a reasonable claim to a specific entry

The Court also noted that under similarly worded VAT entries in several States, the product had been treated as a fruit-based beverage and taxed at concessional rates, thereby reinforcing the plausibility of the appellant’s interpretation. The Court held that the concurrent findings were vitiated by “a clear misdirection in law”.

The Court held that ‘Sharbat Rooh Afza’ was classifiable under Entry 103 of Schedule II, Part A of the UPVAT Act as a fruit drink / processed fruit product and was exigible to VAT at the concessional rate of 4% during the relevant assessment years.

The Court allowed the appeals, set aside the impugned judgments affirming levy at 12.5% under the residuary entry and directed the respondent authorities to grant consequential relief, including refund or adjustment of excess tax paid, in accordance with law.

[Hamdard (Wakf) Laboratories v. Commissioner, Commercial Tax, 2026 SCC OnLine SC 306, decided on 25-2-2026]

*Judgment by Justice R. Mahadevan