The Insolvency and Bankruptcy Code1 (IBC) provides for a time-bound resolution of cases that have been initiated under it. In the initial workings of the IBC, it was popularly reported that the process was marred by delays. The IBC has been in action for a little more than 7 years now and the law, rules and procedures have become much more entrenched with time. This is evidenced by the latest data released by the Economic Survey of India for 2022-2023 (ECI) and the Insolvency and Bankruptcy Board of India (IBBI) showing a significant increase in the efficiency of the National Company Law Tribunal (NCLT).

Latest data shows a total of 7054 corporate insolvency resolution processes (CIRPs) have been initiated till the end of September 2023. Around 45% of cases (2249) have been ordered into liquidation. In comparison, the number of resolution plans approved by NCLT is 808, the rest are pending. Therefore, it can be said that currently, the ratio of resolution to liquidation orders is roughly around 1:3.

In the liquidation cases 77% of cases were pre-IBC legacy cases from Sick Industrial Companies (Special Provisions) Act, 19852 (SICA) and Board for Industrial and Financial Reconstruction (BIFR) and had already been pending for a long period of time. Achieving 23% resolutions in such cases is commendable.

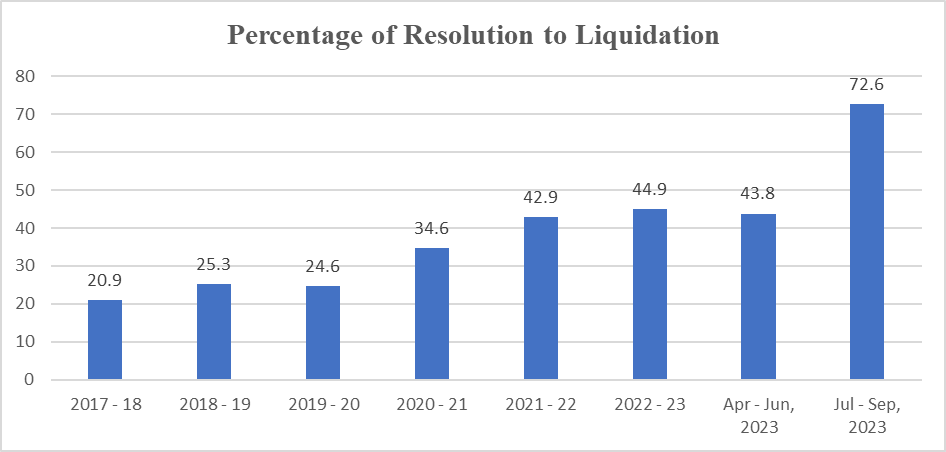

The NCLT has been consistently improving by yielding more resolutions than liquidations, especially if we look at the current data and analyse it in a time series. The graph below shows that the percentage of resolution to liquidation has been consistently improving over time.

Source: IBBI September 2023 Newsletter

IBC has brought in behavioural change and has started positively impacting the credit culture in the country. If the financial institutions are unable to recover a substantial amount of capital from the insolvents, they would instead recover the same from the solvent by hiking the interest rates. This initiates a vicious cycle, where increased interest rates lead to an increase in the cumulative debt, thus pushing solvent businesses towards insolvency. As we can see, the prompt adjudications by the NCLT have been increasingly successful in breaking this trend. As a result, the cost of credit has come down, which has led to increased credit availability, furthering the objectives of the IBC.

The data further shows that a considerable number of companies are also being rescued at the pre-admission stage. Some 26,518 applications having underlying default of Rs 9.33 lakh crores have been withdrawn before admission. This was 3.75 times higher than those (7058 cases) admitted under the IBC.

The IBC also provides for the withdrawal of the CIRP. Till September 2023, a total of 947 CIRPs have been withdrawn. Any withdrawal has to be approved by 90% of the Committee of Creditors (CoC). It can reasonably be assumed that close to full recovery has happened in such cases.

Even during the liquidation stage, there is still a possibility of substantial realisations from the corporate debtor. A scheme under Section 2303 of the Companies Act or the company can be sold as a going concern (GC). As of 31-9-2023, 32 cases were closed as a GC and 8 cases through a Section 230 scheme. In these cases, too, the company is saved, and creditors make substantial realisations, comparable to resolution.

Another significant achievement of the NCLT/IBC is in clawing back more than Rs 5000 crores by resolving 203 preferential, undervalued, extortionate and combination transactions (PUFE). These amounts usually indicate the capital that was siphoned off in a mala fide manner by the erstwhile management of the company by deceiving the creditors who were rightfully owed that money. NCLT by holding such transactions to be PUFE helped return/recovery for the creditors.

The huge haircuts as are reported in the conventional critique of the NCLT, have another perspective, first, the NCLT has no control over the commercial decision of the CoC and second, when the banks take haircuts the amount include massive interest component, which strictly cannot be argued as a loss to the banks. It needs to be understood as a possible profit foregone, instead of a haircut in a sense of loss.

ECI shows that the recovery for scheduled commercial banks through IBC has been the highest for the year ending 2022 compared to all other recovery channels. Banks have clearly benefitted under the IBC regime inasmuch as they make a fresh start with cleaner balance sheets after each insolvency case being resolved.

Apart from insolvency — NCLT also deals with issues under the Companies Act wherein disputes and has to approve transactions, mergers, etc. Considering the number of cases, it is indeed safe to say that NCLT has been performing and delivering at close to optimum levels and the need of the hour is for the appointment of more members to add impetus to the work being done.

†Advocate and a former Partner at Cyril Amarchand Mangaldas. Author can be reached at <bishwajit.dubey@bishwajitdubey.com>.

††Assistant Professor of Law at the National Law University Delhi.

1. Insolvency and Bankruptcy Code, 2016.

2. Sick Industrial Companies (Special Provisions) Act, 1985.