2026 SCC Vol. 5 Part 5: Key Supreme Court Cases on Arbitration, Constitution and IBC

Explore the latest Supreme Court Cases in 2026 SCC Vol. 5 Part 5 on international commercial arbitration, Panchayat elections, corporate debtor, and more.

Bringing you the Best Analytical Legal News

Explore the latest Supreme Court Cases in 2026 SCC Vol. 5 Part 5 on international commercial arbitration, Panchayat elections, corporate debtor, and more.

In this exclusive conversation with Sumant Batra, Insolvency Lawyer, President of the Insolvency Law Academy, and Past President of INSOL International (India),

Explore the latest Supreme Court Cases in 2026 SCC Vol. 5 Part 4 on quasi-judicial authorities, delay in delivery of possession, contract labour, cooperative societies and more.

by Akaant K. Mittal* and Bhavana Garg**

Explore the latest Supreme Court Cases in 2026 SCC Vol. 5 Part 1 on conciliation awards, recording evidence, real estate projects, and more.

The NCLAT held that the NCLT had failed to comply with the mandatory procedural safeguards applicable to contempt proceedings and, therefore, the impugned order could not be sustained. While setting aside the contempt order, the NCLAT also granted certain fact-specific directions in the matter.

Explore the latest Supreme Court Cases in 2026 SCC Vol. 4 Part 2 on demurrer, speculative purchasers, public auction, and more.

Explore the latest Supreme Court Cases in 2026 SCC Vol. 3 Part 5 on voter’s right to know antecedents, rental compensation, jurisdiction of referral court, sale of immovable property, and more.

Section 47-A held inapplicable to statutory and court-supervised auctions, ruling that sale certificates are transfers by operation of law—not conveyances—and cannot be reopened for undervaluation by registering authorities.

Discover the latest legislative updates from April 2026, including all updates on new Central Legislations, Rules, Notifications; and more.

The Court denied the discharge of the company director in a cheque dishonour case wherein the said company was undergoing liquidation.

Explore the latest Supreme Court Cases in 2026 SCC Vol. 2 Part 2 on vesting of private forests, road safety, professional communication, and Aravalli Hills & Ranges.

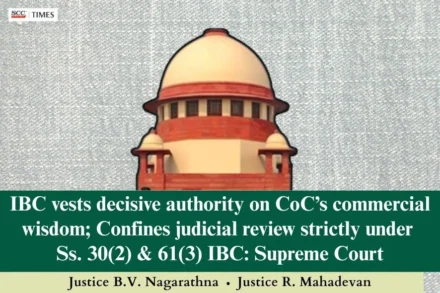

“Commercial wisdom of the CoC enjoys primacy and cannot be supplanted by judicial review. Neither the NCLT, nor the NCLAT nor even this Court is empowered to substitute its assessment in place of the commercial decision arrived at by a requisite majority of the CoC”.