Overview of RBI (Co-Lending Arrangements) Directions, 2025

RBI Co-Lending Arrangements Directions 2025 establish a unified framework for joint lending by banks and NBFCs to improve transparency risk sharing and borrower protection.

Bringing you the Best Analytical Legal News

RBI Co-Lending Arrangements Directions 2025 establish a unified framework for joint lending by banks and NBFCs to improve transparency risk sharing and borrower protection.

The homebuyers’ case was that almost 70-80% of the loan amounts under subvention schemes were disbursed by the banks to the builders-cum-developers as ‘first tranche’, without due diligence, despite project milestones not having achieved.

The matter revolved around the Notification dated 29-05-2015 issued by the Central Government, containing instructions for the Framework for Revival and Rehabilitation of MSMEs.

“Srinivasarao, Senior Advisor, Indian Banks Association is sent notice to appear before the Court on the next date of hearing, i.e., 06-04-2024, so that the stand of all the Banks can be considered.”

Any dilution of the forfeiture provided under Rule 9(5) of SARFAESI Rules would result in entire auction process under SARFAESI Act being disregarded by mischievous auction purchasers through sham bids, thereby undermining the overall object of the Act of promoting financial stability, reducing NPAs and fostering a more efficient and streamlined mechanism for recovery of bad debts.

The right to recovery of the Banks and Financial Institutions if pitted against the constitutional right of life of a person to live with dignity and not to be deprived of without following the established procedure of law, the constitutional rights of the person shall prevail.

‘Audi alteram partem application cannot be impliedly excluded under the Master Directions on Frauds.’

The Supreme Court observed that principles of natural justice should be necessarily read into the provisions of the Master Directions on Frauds, to save it from the vice of arbitrariness.

The PIL seeks formulation and implementation of a scheme that conclusively addresses the grievances of other home buyers who may not have the capacity to approach courts/forums to seek redressal against builders.

The Reserve Bank of India (hereinafter called the Reserve Bank) issued Reserve Bank of India (Unhedged Foreign Currency Exposure) Directions, 2022. These

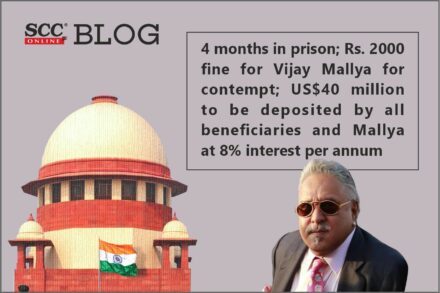

Supreme Court observed that Vijay Mallya “never showed any remorse nor tendered any apology for his conduct” of transferring a huge sum of US$40 million to his children instead of repaying his debt of more than Rs. 9000 crores to the banks.

The Central Government has notified the Assisted Reproductive Technology (Regulation) Rules, 2022 in order to regulate the functioning of Assisted Reproductive Technology

The guidelines on LEI stand extended to Primary (Urban) Co-operative Banks (UCBs) and Non-Banking Financial Companies (NBFCs). The non-individual borrowers enjoying aggregate

Year 2021! The year that started with the hope of the COVID-19 Pandemic nearing an end with countries starting vaccination, ended up

Delhi High Court: Asha Menon, J., expressed that, The Banks seek collaterals and security to prevent losses to themselves. It is, but

Supreme Court: The bench of Ashok Bhushan and MR Shah, JJ has refused to pass any direction in the petition seeking effective

National Company Law Appellate Tribunal (NCLAT): The Division Bench of Justice Anant Bijay Singh, Judicial Member and Shreesha Merla, Technical Member held

There was no justification shown by the Government to restrict the relief of not charging interest on interest with respect to the loans up to Rs. 2 crores only and that too restricted to only 8 categories.

Master Direction on Digital Payment Security Controls The Master Direction provides necessary guidelines for the Regulated Entities (Scheduled Commercial Banks, Small Finance

“Banks cannot wash off their hands and claim that they bear no liability towards their customers for the operation of the locker.”