CAM advises Central Bank of India on joint venture with Generali Participations Netherlands N.V.

Cyril Amarchand Mangaldas acted as legal counsels to Central Bank of India

Bringing you the Best Analytical Legal News

Cyril Amarchand Mangaldas acted as legal counsels to Central Bank of India

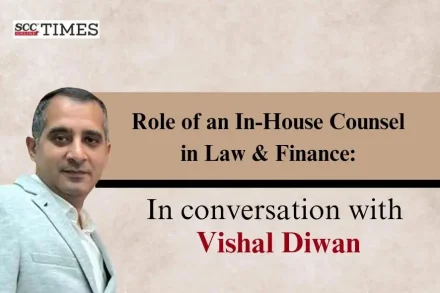

Interviewed by Muskaan Chaube

About RGNUL The Rajiv Gandhi National University of Law, Punjab (RGNUL) is an autonomous National Law University (NLU) established by the RGNUL

While BR Gavai, J has written the majority opinion for himself and SA Nazeer, A.S. Bopanna, V. Ramasubramanian, JJ, to uphold the legality of the 2016 demonetization, BV Nagarathna, J is the lone dissenter who has held that though demonetisation was well-intentioned and well thought of, the manner in which it was carried out was improper and unlawful.

Gujarat National Law University is organizing the 2nd Edition of GNLU International Conference on Business, Law and Public Policy (GICBLP)

Income Tax Appellate Tribunal (ITAT), Bangalore: The coram of N.V. Vasudevan (Vice President) and Padmavathy S. (Accountant Member), considered the instant appeal,

“No doubt, that a Judicial Officer while discharging his/her duties, is expected to be independent, fearless, impassionate and non-impulsive. But a Judicial

Supreme Court: The 3-judge bench of L. Nageswara Rao, Sanjiv Khanna* and BR Gavai, JJ has held that the post office/bank can

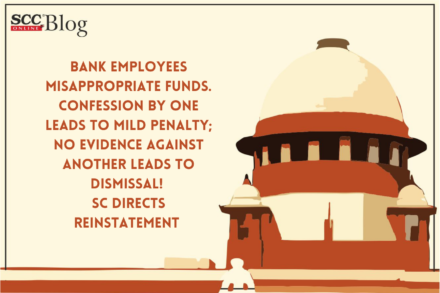

Supreme Court: In a case where a bank employee was dismissed from services despite lack of evidence, the bench of KM Joseph

“A cheque issued as security pursuant to a financial transaction cannot be considered as a worthless piece of paper under every circumstance.”

by Pramod Rao†

Cite as: 2021 SCC OnLine Blog Exp 69

“If an officer/employee of the bank is allowed to act beyond his authority, the discipline of the bank will disappear.”

Under this process, the issuer of the cheque submits electronically, through channels like SMS, mobile app, internet banking, ATM, etc., certain minimum details of that cheque (like date, name of the beneficiary/payee, amount, etc.) to the drawee bank, details of which are cross-checked with the presented cheque by CTS.

Scheme of Amalgamation The Union Cabinet has given its approval to the Scheme of Amalgamation of Lakshmi Vilas Bank Limited (LVB) with

Supreme Court: The 3-Judge Bench of Arun Mishra, B.R. Gavai and Krishna Murari, JJ., set aside the NCLAT’s Order with regard to

Bhumesh Verma, Managing Partner and Paruchuri Baswanth Mohan, Research Associate, Corp Comm Legal

Cite as: (2020) PL (CL) August 60

Supreme Court: The 5-judge bench of Arun Mishra, Indira Banerjee, Vineet Saran, MR Shah and Aniruddha Bose, JJ has held that “’banking’

Supreme Court: Holding the Reserve Bank of India [RBI] Circular issued on 12.02.2018 ultra vires Section 35AA of the Banking Regulation Act,

Supreme Court: The bench of Abhay Manohar Sapre and Indu Malhotra, JJ has held that there cannot be a uniform qualification or/and