Justice Pankaj Mithal Bids Adieu to the Supreme Court: A throwback to His Dedicated Journey & Distinguished Career

Justice Pankaj Mithal began his career in law in the 1980s and subsequently went on to become Judge at the Supreme Court of India.

Bringing you the Best Analytical Legal News

Justice Pankaj Mithal began his career in law in the 1980s and subsequently went on to become Judge at the Supreme Court of India.

“For maintaining an application for default of another Financial Creditor, the essential ingredients to be fulfilled by the Applicant is that the Applicant has to be a Financial Creditor on its own facts.”

Sitting Judge of the Supreme Court of India, Justice Pankaj Mithal began his career in law in the 1980s and subsequently went on to become Chief Justice of High Courts of J&K and Ladakh and Rajasthan.

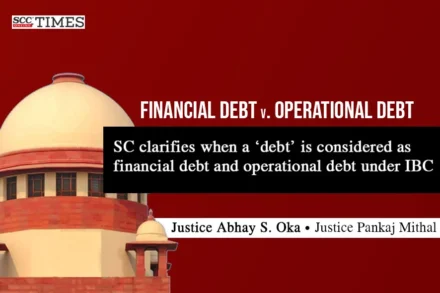

Noting that hypothecation means the process of using an asset as collateral for a loan. It acts as a protection to the lender when the borrower does not repay the loan, the Supreme Court highlighted that the name of the document is not a decisive factor. Only because the title of the document contains the word hypothecation, it cannot be concluded that guarantee is not a part of this document.

The NCLAT reinforced that not all financial transactions qualify as financial debts under the IBC.

by Sidharth Sethi† and Shreya Sircar††

Sitting Judge of the Supreme Court of India, Justice Pankaj Mithal began his tryst with law in the 1980s.

The application is filed by Jammu and Kashmir Bank against the Himalayan Mineral Waters Private Limited for a total financial debt of Rs. 50,04,38,456/- for the credit facilities availed by Leel Electricals.

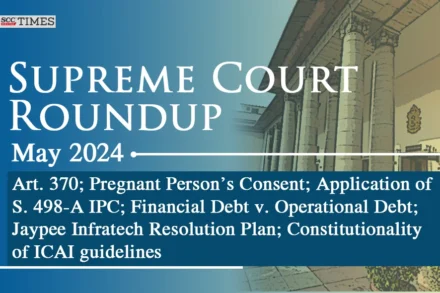

The roundup revisits the analyses of Supreme Court’s judgments/orders on Pregnant person’s consent; Application of S. 498-A IPC; Financial Debt v. Operational Debt and more. It also covers the top stories; Never reported Judgments and Know thy Supreme Court Judges.

“While deciding that whether a debt is a financial debt or an operational debt arising out of a transaction covered by an agreement or arrangement in writing, it is necessary to ascertain what is the real nature of the transaction reflected in the writing.”

The NCLAT reiterated the importance of adhering to timelines in the Insolvency resolution process and the unacceptability of claims filed after the approval of the Resolution Plan by the CoC.

NCLT’s order did not contain specific findings regarding whether the entire loan amount had been paid and whether nothing remained due.

Amount taken by the Directors of the Corporate Debtor in their personal capacity cannot be construed as ‘Financial Debt’ under S. 5(8) of the IBC.

In the instant matter an appeal was preferred against the order of NCLT admitting S. 7 IBC application or repayment of financial debt. Upholding the order of the NCLT, the Tribunal held that even if there is no proof of loan agreement other materials on record can prove the financial debt.

by Kartikey Mahajan, Siddhant Sharma and Jatan Rodrigues

Cite as: 2022 SCC OnLine Blog Exp 87

National Company Law Tribunal, New Delhi: The bench of Abni Rajan Kumar Sinha, Judicial Member and Hemant Kumar Sarangi, Technical Member has

National Company Law Tribunal, Allahabad (NCLT): The bench of Rajasekhar V.K., Judicial Member and Virendra Kumar Gupta, Technical Member decided that for

Supreme Court: The 3-judge bench of L. Nageswara Rao, BR Gavai* and AS Bopanna, JJ has held that a liability in respect

National Company Law Tribunal, New Delhi: The Coram of P.N. Prasad, Judicial Member and Rahul Bhatnagar, Technical Member, declared insolvency proceedings against