Introduction

A consumer complaint filed by my firm in the month of March 2023 had been flagged by the Registry as being time-barred. In our case, the right to file the complaint first arose on 21-1-2020. In the opinion of the District Consumer Commission, the limitation period in our case would have normally expired on 20-1-2022 but that owing to para 5.3 of Cognizance for Extension of Limitation, In re, order dated 10-1-20221 (hereinafter “the 10-1-2022 order”), the limitation period in our case expired on 30-5-2022 (i.e. ninety days from 1-3-2022). The above episode makes it evident that there is a belief prevailing in at least some quarters of the Bar that all litigants, whose prescribed limitation period to institute a proceeding expired between 15-3-2020 and 28-2-2022, only had a limitation period of ninety (90) days with effect from 1-3-2022 to institute their proceeding and on their failure to institute the same within 30-5-2022, their right to institute such proceeding becomes time barred. I shall hereinafter refer to this belief, argument or understanding, as “the 90-day limitation rule”.

To the eyes of reason, the 90-day limitation rule just cannot follow from the 10-1-2022 order for grounds which are evident from the face of the 10-1-2022 order itself. Para 5.3 of the 10-1-2022 order contains two stipulations. The first stipulation is to the effect that “in cases where the limitation would have expired between 15-3-2020 and 28-2-2022, then notwithstanding the actual balance period of limitation remaining, all persons shall have a limitation period of 90 days from 1-3-2022”. The second stipulation in para 5.3 is to the effect that in the cases referred to in the first stipulation, “if the actual balance period of limitation remaining with effect from 1-3-2022 is greater than 90 days, that longer period shall apply”.2 The second stipulation is quite clearly designed to operate as an exception to the first stipulation because its very nature reveals that it can have no other purpose in the 10-1-2022 order.

An application of the two stipulations in para 5.3 to my firm’s consumer case described earlier would be as follows: The prescribed limitation period terminated on 20-1-2022 and thus it falls within the contours of the first stipulation. The effect of the exception in the second stipulation must also be determined but the 90-day limitation rule confines itself to the question whether limitation expired between 15-3-2020 and 28-2-2022 and takes no account of the balance limitation period as on 1-3-2022. However, in the application of the second stipulation, there is a logical impossibility. How could my case whose prescribed limitation terminated on 20-1-2022 have any balance period of limitation on 1-3-2022? On the same note, how could any case whose prescribed limitation expired between 15-3-2020 and 28-2-2022 have any balance period of limitation with effect from 1-3-2022? Did the Supreme Court make a mistake here?

No. The answer is in para 5.2. Para 5.2 stipulates explicitly that whatever balance period of limitation was remaining as on 3-10-2021 is carried forward and made available with effect from 1-3-2022.3 Therefore, whatever number of days were available as balance limitation period as on 3-10-2021 were carried forward and made available on 1-3-2022. But there is one more hiccup. Suppose my balance limitation period as on 3-10-2021 was greater than 90 days and this greater period was transposed to 1-3-2022. Would I only be left with a limitation period of 90 days as on 1-3-2022? The 90-day limitation rule wants us to believe so. But if it were so, it would mean that the Supreme Court carried forward the entire balance limitation period as on 3-10-2021 to 1-3-2022 in para 5.2 only to partially retract it and dilute it to 90 days in the very next paragraph which is ex facie untenable. Moreover, the second stipulation in para 5.3 stipulates explicitly that in case the balance limitation period as on 1-3-2022 is greater than 90 days, the longer period shall apply.

In case the Supreme Court intended to frame a blanket of 90-day limitation period for all cases whose limitation expired between 15-3-2020 and 28-2-2022, the Supreme Court would have stated so in categorical terms rather than excluding the period from 15-3-2020 till 28-2-2022 for limitation computation in para 5.1, carrying forward balance limitation period from 3-10-2021 to 1-3-2022 in para 5.2 and also creating an exception to the 90day limitation period applicability in para 5.3. As shown in the above analysis, the 90-day limitation rule is based on a myopic approach to the 10-1-2022 order as it fails to take into account the exception in para 5.3 or the exclusion and carry forward stipulations in paras 5.1 and 5.2. But being easily prone to misinterpretation, the 90-day limitation rule can derail the entire scheme and purpose of the 10-1-2022 order by causing the incorrect disqualification of proceedings as time-barred or by needlessly necessitating expenditure of judicial time in appeal or revision proceedings on this very issue which I and surely others will find troubling.

To assuage this concern, I have undertaken to comprehensively study the entire purport of the 10-1-2022 order so as to ascertain its true operative effect as applicable to its varied permutations and herewith I have presented my observations to the interested reader. Ordinarily, judicial decisions cannot be relied on to predict or reduce legal outcomes to a mathematical certainty for no two facts can be identical. However, the Cognizance for Extension of Limitation, In re orders did not concern themselves with the appreciation of factual issues as in ordinary cases but had a singular purpose i.e. to issue computational directions4 for the computation of available limitation period to applicable cases given that the pandemic adversely affected the normal operation of the courts forcing the extension of limitation period. Since the application of computational directions issued by the Supreme Court in the 10-1-2022 order involve fairly basic operations of a mathematical nature, it must be possible to ascertain the operative effect of the 10-1-2022 order to a mathematical certainty and this formed the object of my enquiry. In the 10-1-2022 order, the Supreme Court made a reference5 to its earlier orders dated 23-3-20206, 8-3-20217, 27-4-20218 and 23-9-20219 which were also passed under the same case title. In this work, these orders shall be referred to simply as the 23-3-2020 order, 8-3-2021 order, 27-4-2021 order and the 23-9-2021 order, respectively. References in this work to “prescribed limitation period” shall mean that limitation period which would have been ordinarily applicable in respect of any proceeding in case none of the above Cognizance of Extension of Limitation, In re10 orders were passed by the Supreme Court.

Balance period of limitation on 1-3-2022

The operation of the 10-1-2022 order boils down to one question i.e. what is the balance period of limitation as on 1-3-2022? For cases whose prescribed limitation expired between 15-3-2020 and 28-2-2022, if the balance limitation period as on 1-3-2022 was greater than 90 days, then the greater period was available as limitation from 1-3-2022 but if lesser than 90 days, then a blanket 90-day limitation period was available from 1-3-2022. For cases whose prescribed limitation was to expire after 28-2-2022, the balance period of limitation as on 1-3-2022 was available as limitation. As seen earlier, there is a nuance to ascertaining which cases had balance period of limitation as on 1-3-2022 and also in ascertaining the extent of balance limitation period that is actually available for such cases from 1-3-2022.

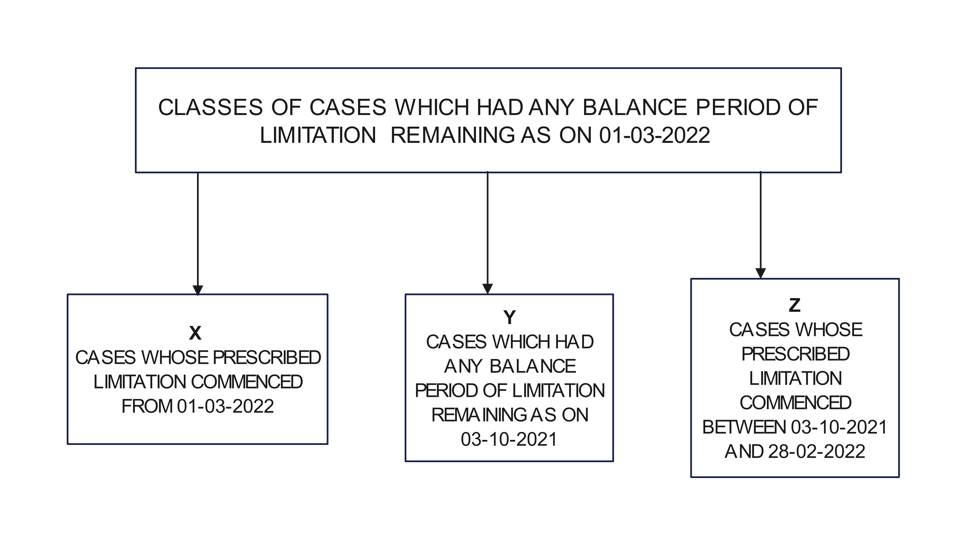

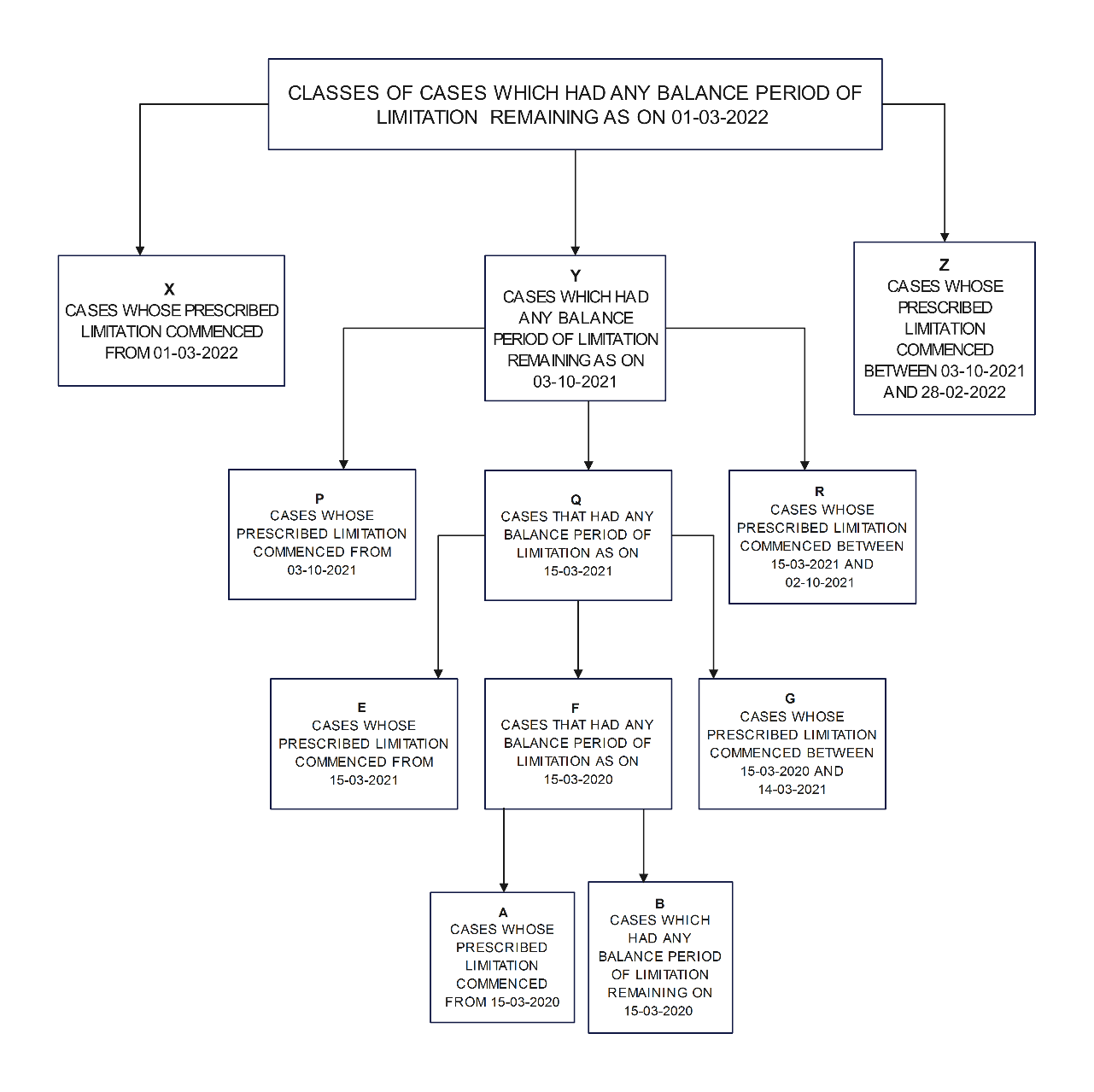

Three classes of cases can have some balance period of limitation remaining as on 1-3-2022. The cases where the prescribed period of limitation itself commenced on 1-03-2022 will obviously have the entire limitation period available as balance limitation period from 1-3-2022. I shall classify these cases as the X type of cases. By the operation of para 5.2 of the 10-1-2022 order, cases that had any balance period of limitation as on 3-10-2021 had that entire balance limitation period carried forward and made available with effect from 1-3-2022 and these cases, I shall classify as the Y type of cases.

Apart from the above two classes, there is another class of cases where the prescribed limitation period would have started running between 3-10-2021 and 28-2-2022. By the operation of para 5.1, the period from 3-10-2021 to 28-2-2022 has been excluded for limitation computation purposes and this exclusionary effect formed the causal basis11 for the carrying forward of the balance limitation period remaining as on 3-10-2021 to 1-3-2022. Therefore, if the period from 3-10-2021 to 28-2-2022 is excluded for limitation computation and the balance limitation period as on 3-10-2021 is transposed to 1-3-2022, it must follow that the period from 4-10-2021, 5-10-2021, 6-10-2021 and so on up to 28-2-2022 would also be excluded for limitation computation purposes and the balance limitation period as on 4-10-2021, 5-10-2021, 6-10-2021 and so on up to 28-2-2022 would also be carried forward and made available on 1-3-2022 for the exclusion of the period from 3-10-2021 till 28-2-2022 for limitation computation purposes can have no other meaning. Therefore, in such cases, the commencement of the entire limitation period would be deferred up to 1-3-2022. For such cases whose prescribed limitation period started running between 3-10-2021 and 28-2-2022, I shall classify them as the Z type of cases. Therefore, X, Y, and Z are the only classes of cases that can have any balance limitation period as on 1-3-2022 as in the flow diagram below. But our enquiry cannot end here.

Balance period of limitation as on 3-10-2021

The Y class of cases are those that had some balance period of limitation as on 3-10-2021 which balance got transposed to 1-3-2022 by the operation of para 5.2 of the 10-1-2022 order. 3-10-2021 is a pertinent date in our enquiry because the Supreme Court passed the 23-9-2021 order wherein the period from 15-3-2020 till 2-10-2021 was excluded for limitation computation purposes and the balance period of limitation as on 15-3-2021 was carried forward and made available as balance limitation period with effect from 3-10-202112. The 23-9-2021 order has a bearing on the 10-1-2022 order because para 5.1 of the 10-1-2022 order stipulates explicitly that the 10-1-2022 order is “in continuation” with the 23-9-2021 order13. The operative portion of the 23-9-2021 order contains stipulations identical to the 10-1-2022 order. Para 9(I) of the 23-9-2021 order excludes the period from 15-3-2020 till 2-10-2021 for limitation computation purposes and also carries forward the balance limitation period remaining as on 15-3-2021 to 3-10-202114.

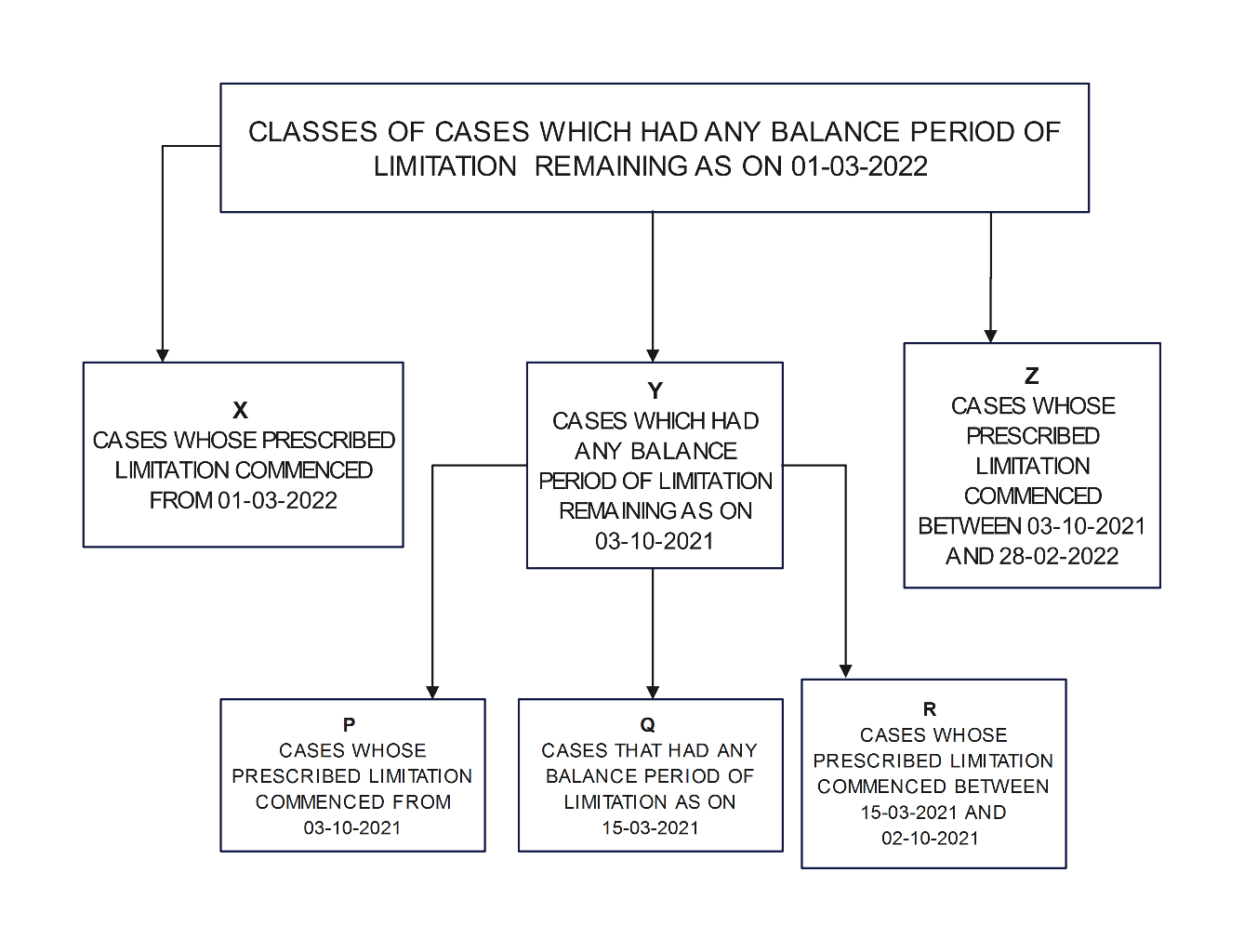

Akin to X, Y, and Z classes of cases seen earlier, there are three classes of cases which could have some balance period of limitation remaining as on 3-10-2021. The first class would comprise of cases whose prescribed limitation started running from 3-10-2021 which I shall classify as the P type of cases. Second are the cases which had any balance period of limitation as on 15-3-2021 and which balance got carried forward to 3-10-2021 by the operation of para 9(I) of the 23-9-2021 order and I shall classify such class of cases as the Q type of cases.

Akin to the Z class of cases, there would be another class of cases where the prescribed limitation started running in the excluded period between 15-3-2021 and 2-10-2021. The carry forward of the balance limitation period as on 15-3-2021 to 3-10-2021 in the 23-9-2021 order is the causal effect15 of the exclusion of the period from 15-3-2021 to 2-10-2021 for limitation computation purposes in para 9(I) of the 23-9-2021 order. Therefore, if the period from 15-3-2021 till 2-10-2021 is excluded for limitation computation and the balance limitation period as on 15-3-2021 is transposed to 3-10-2021, it must follow that the period from 16-3-2021, 17-3-2021, 18-3-2021 and so on up to 2-10-2021 would also be excluded for limitation computation purposes and the balance limitation period as on 16-3-2021, 17-3-2021, 18-3-2021 and so on up to 2-10-2021 would also be carried forward and made available on 3-10-2021 for the exclusion of the period from 15-3-2021 till 2-10-2021 for limitation computation purposes can have no other meaning. Therefore, in such cases, the commencement of the entire limitation period would be deferred up to 3-10-2021. Such cases whose prescribed limitation period started running between 15-3-2021 and 2-10-2021, I shall classify them as the R type of cases. Therefore, the P, Q, and R are the only classes of cases that can have any balance period of limitation as on 3-10-2021 and together they constitute the Y class of cases. After incorporating the operative stipulations of the 23-9-2021 order, the updated flow diagram showing cases that had balance period of limitation as on 1-3-2022 is as under:

Balance period of limitation as on 15-3-2021

Our enquiry must continue. The Q class of cases are cases that had some balance period of limitation as on 15-3-2021 which got transposed to 3-10-2022 by the operation of para 9(I) of the 23-9-2021 order. 15-3-2021 is a pertinent date for the purposes of our enquiry because the Supreme Court passed the 8-3-2021 order wherein the period from 15-3-2020 till 14-3-2021 was excluded for limitation computation purposes and the balance limitation period remaining as on 15-3-2020 was made available as balance limitation period from 15-3-2021.16 The 8-3-2021 order has a bearing on the 10-1-2022 order because para 5.1 of the 10-1-2022 order stipulates explicitly that the 10-1-2022 order is “in continuation” also with the 8-3-2021 order.17 The operative portion of the 8-3-2021 order contains stipulations identical to the 23-9-2021 and 10-1-2022 orders. Para 2.1 of the 8-3-2021 order excludes the period from 15-3-2020 till 14-3-2021 for limitation computation purposes and also carries forward the balance limitation period remaining as on 15-3-2020 to 15-3-2021.18

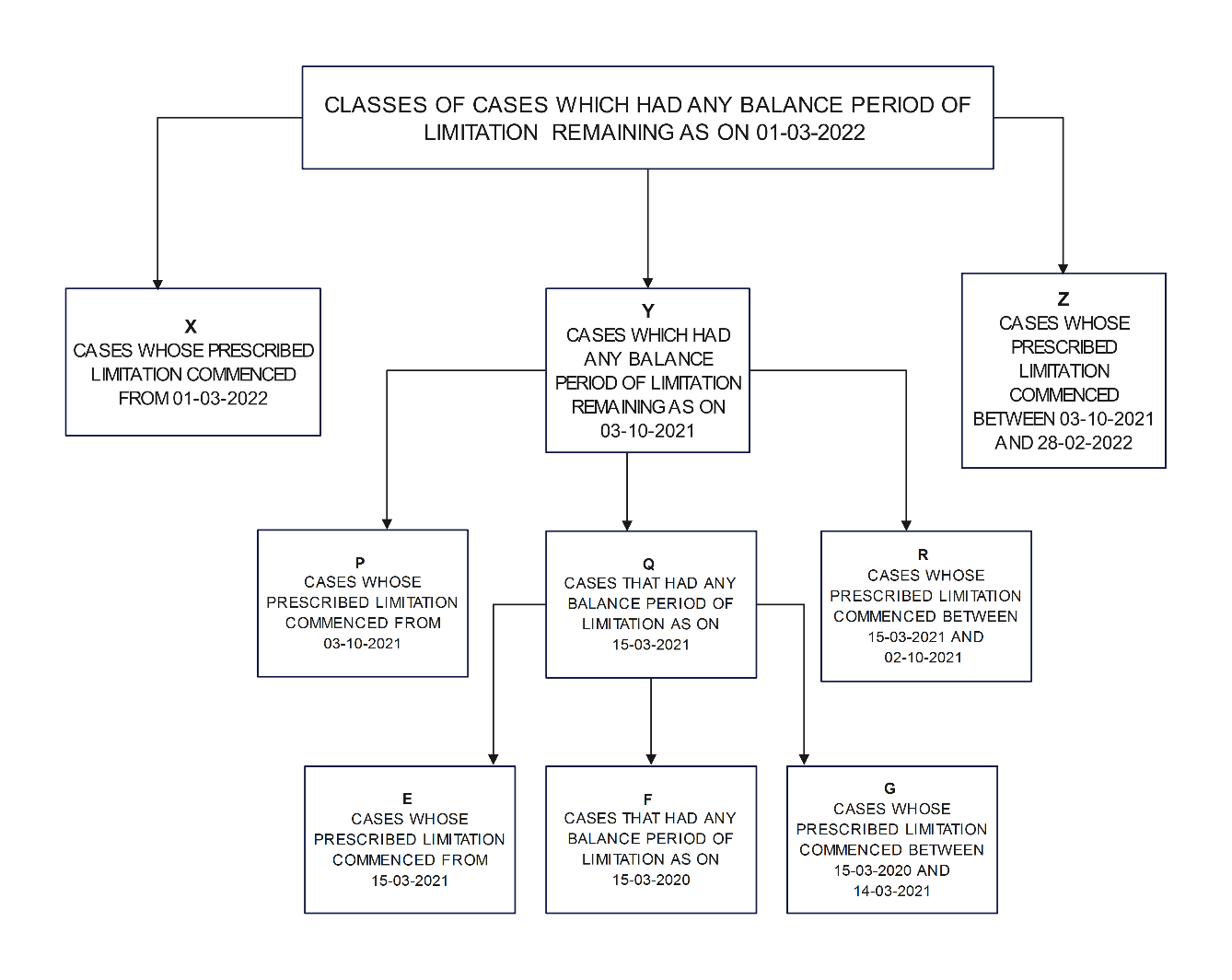

Akin to X, Y, Z, P, Q and R classes of cases, there are three classes of cases that could have some balance period of limitation remaining as on 15-3-2021. First are the cases whose prescribed period of limitation started running from 15-3-2021 which Class I shall classify as E type of cases. Second are the cases which had any balance period of limitation as on 15-3-2020 and which got carried forward to 15-3-2021 by the operation of para 2.1 of the 8-3-2021 order and I shall classify them as the F class of cases.

Third are the cases whose prescribed limitation started running between 15-3-2020 and 14-3-2021. Para 2.1 of the 8-3-2021 order excluded the period from 15-3-2020 till 14-3-2021 for limitation computation purposes and also carried forward the balance limitation period remaining as on 15-3-2020 and made it available on 15-3-2021. The carry forward of the balance limitation as on 15-3-2020 to 15-3-2021 is a direct causal effect19 of the exclusion of the period from 15-3-2020 till 14-3-2021 for limitation computation purposes. Therefore, if the period from 15-3-2020 to 14-3-2021 is excluded for limitation computation and the balance limitation period as on 15-3-2020 is transposed to 15-3-2021, it must follow that the period from 16-3-2020, 17-3-2020, 18-3-2020 and so on up to 14-3-2021 would also be excluded for limitation computation purposes and the balance limitation period as on 16-3-2020, 17-3-2020, 18-3-2020 and so on up to 14-3-2021 would also be carried forward and made available on 15-3-2021 for the exclusion of the period from 15-3-2020 till 14-3-2021 for limitation computation purposes can have no other meaning. Therefore, in such cases, the commencement of the entire limitation period would be deferred up to 15-3-2021. Such cases whose prescribed limitation period started running between 15-3-2020 and 14-3-2021, I shall classify them as the G type of cases. Therefore, the E, F, and G classes of cases are the only classes of cases that can have any balance period of limitation as on 15-3-2021 together they constitute the Q class of cases. After incorporating the operative stipulations of the 8-3-2021 order, the updated flow diagram showing cases that had balance period of limitation as on 1-3-2022 is as under:

Balance period of limitation as on 15-3-2020

The F class of cases are those which had any balance period of limitation as on 15-3-2020. Two classes of cases can have balance period of limitation as on 15-3-2020. First are the cases whose prescribed limitation started running from 15-3-2020 which Class I shall classify as the A type of cases. Second are the cases whose prescribed limitation started running prior to 15-3-2020 and which had some balance period of limitation yet to be run out as on 15-3-2020 and this Class I shall classify as the B type of cases. The A and B classes of cases are the only class of cases that can have any balance period of limitation remaining as on 15-3-2020 and whatever balance limitation period was available to these cases as on 15-3-2020 was carried forward to 15-3-2021 by the operation of para 2.1 of the 8-3-2021 order and A and B classes of cases together constitute the F class of cases. After incorporating the A and B classes of cases, the updated flow diagram showing cases that had balance period of limitation as on 1-3-2022 is as under:

Cumulative operative effect of the 10-1-2022 order

Para 5.1 of the 10-1-2022 order stipulates inter alia that the 10-1-2022 order is “in continuation” of the 8-3-2021 and 23-9-2021 orders.20 The 8-3-2021, 23-9-2021 and the 10-1-2022 orders evidence a scheme of exclusion and carry forward of balance limitation periods in a remarkably synchronous manner.

|

Order |

Para No. |

Period excluded for limitation computation |

Balance transposed |

Carry forward of balance limitation period |

|

8-3-2021 |

2.1 |

15-3-2020 till 14-3-2021 |

15-3-2020 to 15-3-2021 |

A + B → F |

|

23-9-2021 |

9(I) |

15-3-2020 till 2-10-2021 |

15-3-2021 to 3-10-2021 |

E+F+G → Q |

|

10-1-2022 |

5.1 & 5.2 |

15-3-2020 till 28-2-2022 |

3-10-2021 to 1-3-2022 |

P+Q+R →Y |

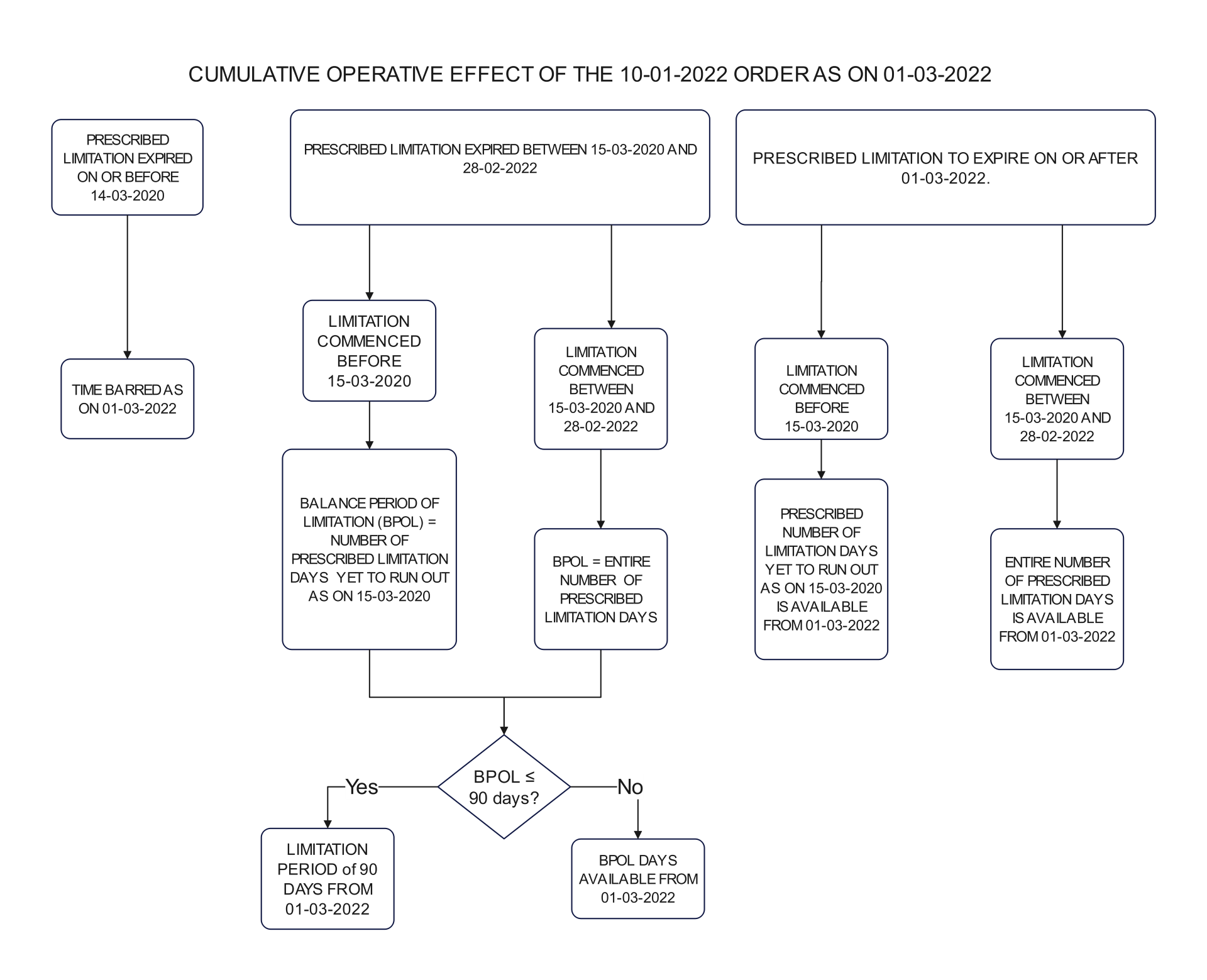

Therefore, it is evident that A and B classes of cases had their balance limitation period as on 15-3-2020 transposed to 15-3-2021 and formed the F class of cases. The E, F, and G classes of cases had their balance limitation period remaining as on 15-3-2021 transposed to 3-10-2021 forming the Q class of cases. The P, Q, and R classes of cases had their balance limitation period remaining as on 3-10-2021 transposed to 1-3-2022 forming the Y classes of cases. As on 1-3-2022, the A and B cases had their balance limitation period as on 15-3-2020 transposed to 1-3-2022 by getting subsumed into the F, Q, and Y classes of cases and the entire prescribed limitation period for the E, G, P, R and Z classes of cases got carried forward and became available on 1-3-2022 by the combined operation of para 2.1 of the 8-3-2021 order, para 9(I) of the 23-9-2021 order and para 5.1 of the 10-1-2022 order. The computation of limitation as on 1-3-2022 in all cases where the 10-1-2022 order has a bearing is as in the following flowchart model:

The cumulative operative effect of the 10-1-2022 order as in the above computational model is consistent with every stipulation in the 10-1-2022 order and accomplishes but the stated intent of the 10-1-2022 order which is this: The absolute exclusion of the period from 15-3-2020 to 28-2-2022 for limitation computation purposes. The effect of such exclusion would naturally result in the deferred running of the prescribed limitation period. The Supreme Court has made this outcome emphatically clear by not only excluding the period from 15-3-2020 to 28-2-2022 for limitation computation but also carrying forward the any balance limitation not having run in the excluded period to 1-3-2022.

Pertinently, in Prakash Corporates v. Dee Vee Projects Ltd.21, the Supreme Court while discussing the exclusionary effect of the 8-3-2021 order observed that:

When a period is excluded for limitation, the excluded period results in enlargement of time over and above the period prescribed and the rationale underlying such exclusion is that the litigant cannot be faulted for not instituting his proceeding in such period for he was prevented by force of circumstances or other requirements of law from so instituting.

In yet another decision22 relating to the exclusionary effect of Section 1423 of the Limitation Act, it has been held that when a certain time period is excluded in computing the limitation period, the days excluded have to be added to what is primarily the prescribed limitation.

Conclusion

The Cognizance for Extension of Limitation, In re24 orders were passed during tumultuous times in our nation’s history. The pandemic took at least half a million Indian lives, threatened the breakdown of the healthcare delivery system, and threw everything out of normalcy. Combating the virus called for medical measures, police measures and also legal measures as laws were invoked or created to enforce lockdowns, to regulate movement, to regulate entry and exit from acutely infected homes and colonies, to regulate supply of essential commodities and services, track covid spread, to ease threshold for invoking insolvency provisions, to introduce moratorium for loans, to ease income tax provisions, etc. All rules have exceptions and when exceptional times called for deviations from ordinary limitation rules, the Supreme Court for its part carved out exceptions to the limitation laws by formulating the above computational directions. In the first wave of the pandemic, the 23-3-2020 order paused the limitation clock indefinitely from 15-3-2020. The 8-3-2021 order resumed the limitation clock from 15-3-2021 and in doing so excluded the entire period from 15-3-2020 till 14-3-2021 for limitation computation purposes. The second wave of the pandemic forced the Supreme Court to pass the 27-4-2021 order once again pausing the limitation clock indefinitely from 14-3-2021. The 23-9-2021 order resumed the limitation clock from 3-10-2021 and in doing so excluded the entire period from 15-3-2020 till 2-10-2021 for limitation computation purposes. The third wave of the pandemic forced the Supreme Court to pass the 10-1-2022 order wherein the period from 15-3-2020 till 28-2-2022 was excluded for limitation computation purposes. As if to negate any doubt on the exclusionary effect the Supreme Court ensured that any prescribed limitation period that may have ordinarily ensued in the excluded period from 15-3-2020 till 28-2-2022 was not counted as having run and was instead carried forward as balance limitation period remaining making it available as balance limitation period in full from 1-3-2022 onwards. Further, even in cases where the carried forward balance limitation period was less than 90 days, a benevolent allowance of 90-day limitation period was made. The above being the case, unless the language of English itself underwent a monumental epistemological shift in the brief intervening period, the 90-day limitation rule is the farthest outcome the Supreme Court could have intended.

* Advocate, Thomas & Associates, Chennai. LLB (Hons) from IIT Kharagpur. Author can be reached at davidsondevashish@gmail.com.

2. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, 119.

3. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, 119.

4. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452; Cognizance of Extension of Limitation, In re, 2021 SCC OnLine SC 947; and Cognizance of Extension of Limitation, In re, (2022) 3 SCC 117; stipulate expressly that the directions stated therein are for the purposes of limitation computation.

5. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, 119.

6. Cognizance for Extension of Limitation, In re, (2020) 19 SCC 10.

7. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452.

8. Cognizance for Extension of Limitation, In re, 2021 SCC OnLine SC 373.

9. Cognizance for Extension of Limitation, In re, 2021 SCC OnLine SC 947.

10. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452; Cognizance of Extension of Limitation, In re, 2021 SCC OnLine SC 947; Cognizance of Extension of Limitation, In re, (2022) 3 SCC 117.

11. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, paras 5.1-5.2; this order evidences that the carry forward of the balance limitation period as on 3-10-2021 to 1-3-2022 is “consequent” upon the exclusion of the period from 15-3-2020 till 28-2-2022 for limitation purposes.

12. Cognizance for Extension of Limitation, In re, 2021 SCC OnLine SC 947.

13. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, 119.

14. Cognizance for Extension of Limitation, In re, 2021 SCC OnLine SC 947.

15. Cognizance for Extension of Limitation, In re, 2021 SCC OnLine SC 947, para 9(I); order evidences that the carry forward of the balance limitation period as on 15-3-2021 to 3-10-2021 is “consequent” upon the exclusion of the period from 15-3-2020 till 2-10-2021 for limitation purposes.

16. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452, 453.

17. Cognizance for the Extension of Limitation, In re, (2022) 3 SCC 117, 119.

18. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452, 453.

19. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452, para 2.1; this order evidences that the carry forward of the balance limitation period as on 15-3-2020 to 15-3-2021 is “consequent” upon the exclusion of the period from 15-3-2020 till 14-3-2021 for limitation purposes.

20. Cognizance for Extension of Limitation, In re, (2022) 3 SCC 117, 119.

22. Kali Prasad Mahton v. Santlal Mahton, 1957 SCC OnLine Pat 39.

24. Cognizance for Extension of Limitation, In re, (2021) 5 SCC 452; Cognizance of Extension of Limitation, In re, 2021 SCC OnLine SC 947; Cognizance of Extension of Limitation, In re, (2022) 3 SCC 117.