Primacy to Suraksha: Understanding the Bharatiya Nagarik Suraksha Sanhita, 2023

The BNSS adopts a “citizen-centric” approach, balancing the rights of both the victims and the accused, respecting the human rights principles.

Bringing you the Best Analytical Legal News

The BNSS adopts a “citizen-centric” approach, balancing the rights of both the victims and the accused, respecting the human rights principles.

The practice and procedure, both pre and post GST are consistent and involve participation of the officer of the DGGI in issuance of show cause notices.

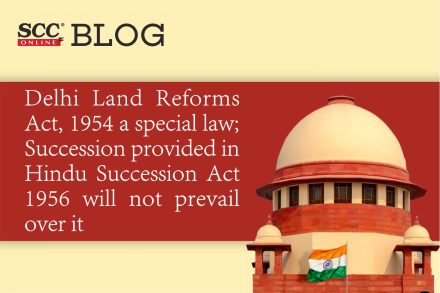

Supreme Court: In a case where challenge was made to declare Section 50(a) of the Delhi Land Reforms Act, 1954 unconstitutional being

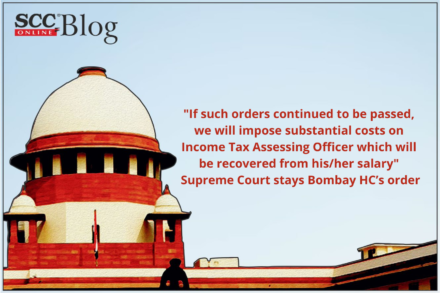

Supreme Court: The Division Bench comprising of M.R. Shah and B.V. Nagarathna, JJ., stayed the impugned order of Bombay High Court wherein

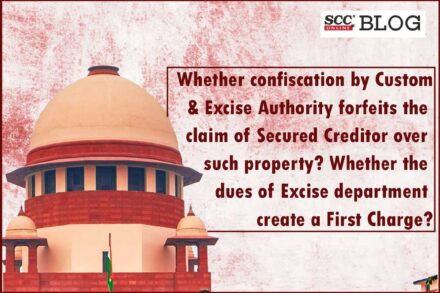

Supreme Court: The Division Bench of L. Nageswara Rao and Vineet Saran*, JJ., quashed the confiscation order of Customs and Central Excise

Supreme Court: The Division Bench comprising of M. R. Shah* and Sanjiv Khanna, JJ., reversed the impugned order of the High Court

“One can imagine the serious hardship that would be caused to the consumers, if cases which have been already instituted before the NCDRC were required to be transferred to the SCDRCs as a result of the alteration of pecuniary limits by the Act of 2019.”

by Jatin Sehgal* & Shailesh Poddar**

Supreme Court: The Bench of J. Chelameswar and Abhay Manohar Sapre, JJ said that no right or liability can be created by