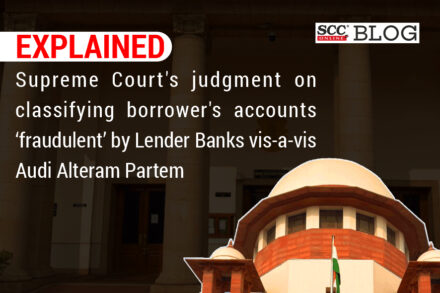

Builder Received Home Loan Amount, Defaulted on Repayment, Yet SBI Proceeded Against Homebuyers: Rajasthan RERA Steps In and Restrains Coercive Recovery

The authority restrained the respondents from carrying on or continuing any action detrimental to the complainants’ interests in respect of the 2 flats and directed SBI not to take any coercive action against the complainants for recovery of the amount.