Introduction: The mens rea pendulum

In describing the exponential growth of information, Tobin Hart very interestingly refers to this as the silicon age of information, where everyone has access to information about everything from pipe bombs to prophecy.1 And yet, the theory of asymmetric information2 that proposes imbalances of information between buyers and sellers leading to market failure still holds. Even the average Joe would have come to hear of the trial of Rajat Gupta for insider trading, who famously received sentencing support from Bill Gates, Kofi Annan, and many more.3

While “insider” and “trading” have been defined separately, “insider trading” as a phrase does not find mention in the governing piece of legislation in India i.e. the SEBI (Prohibition of Insider Trading) Regulations, 2015 (2015 PIT)4. To quote the High-Level Committee5, insider trading loosely refers to “the wrong of trading in securities with the advantage of having asymmetrical access to unpublished information, which, when published, would impact the price of securities in the market (UPSI)”.6 Insider trading violates two core objectives of securities regulation endorsed by the International Organisation of Securities Commissions (IOSCO): “protecting investors and ensuring that markets are fair, efficient, and transparent” .7 The same is also violative of the foremost objective of the SEBI Act, 1992.8

It is true that most insider trading cases are run-of-the-mill in terms of existing precedent which obviates the need for Judges to dig deeply into the doctrinal weeds. However, we often encounter puzzles in the law that remind us how elusive its first principles can be. A current issue that has polarised and puzzled many is the significance of a “profit motive” while pinning down the existence of insider trading. It is interesting to trace how the pendulum has historically swung on including and excluding motive in insider trading offences.

A. Low-down on history

There have been instances where the appellate authority constituted by the Central Government determined a case to be one of insider trading under Regulation 3(1) of the SEBI (Prohibition of Insider Trading) Regulations, 1992 (1992 PIT),9 when an appellant argued that proof of insider trading offence must also show a profit, a benefit, or a purpose of seeking an advantage.10 This was back when the Securities Appellate Tribunal (SAT) was not yet functional and the ad hoc appellate authority consisted of the then Finance Secretary and the Special Secretary (Banking).11 It held that profiting or avoiding loss is not essential for bringing an insider trading charge.

This seems to have reverberated in the Bombay High Court halls, as seen in the 2004 judgments SEBI v. Cabot International Capital Corpn.12 and SEBI v. SKDC Consultants Ltd.13 delivered by the same Bench of Judges in a span of just nine days. However, also in 2004, in Rakesh Agrawal v. SEBI14, the SAT overturned the respondent’s act of holding the appellant guilty of insider trading. By literally interpreting Regulation 3 of the 1992 PIT15, SEBI had identified mens rea as not crucial for conviction. On the contrary, the SAT found that the true spirit of the SEBI Regulations was disregarded by respondent’s interpretation and held mens rea to be essential.

It observed that “while it is true that the regulation does not specifically bring in mens rea as an ingredient of insider trading. But that does not mean that the motive needs to be ignored”.16 Accounting for Rakesh Agrawal’s mens rea, the SAT absolved him of liability. It ruled that interpreting his decision to tender his shares in the public offering at a price higher than what he had initially bought them for as an attempt to obtain an unfair advantage over other shareholders was impossible. The gain merely served as a byproduct of the intended goal to increase his company’s interest.17

Credits are due to SEBI v. Abhijit Rajan (Abhijit Rajan)18, which rekindled this somewhat settled debate in 2022 by reading the insider’s profit motive into the 1992 PIT.19 After confirming SEBI v. Kanaiyalal Baldevbhai Patel20, the Supreme Court noted that mens rea is dispensable for insider trading offences. Instead, it held that the Court should consider the insider’s “profit motive”. With this, reading mens rea into the offence of insider trading is out of the question.

Despite differentiating the terms “profit motive” and mens rea, the Court has failed to highlight the same in a substantial manner. At its core, “profit motive” is the intention to profit at another’s expense, with the knowledge that such act constitutes the offence of insider trading. If anything, the distinction is artificial with no difference in actuality. Therefore, the relevance of “profit motive” in insider trading convictions still looms. The authors seek to explore this issue considering current legal precedents, discussions by numerous expert panels, and a global perspective to churn out a workable solution.

The birth of the “profit motive” standard in Abhijit Rajan

Mr Abhijit Rajan was the Managing Director and Chairman of Gammon Infrastructure Projects (GIPL) which received a contract from the National Highways Authority of India (NHAI) in 2012.21 Similarly, the NHAI awarded another contract to Simplex Infrastructure Limited (SIL).22 Both entities set up special purpose vehicles (SPV) to execute respective projects and drew up shareholders’ agreements (SHA) whereby both entities were to acquire a 49% stake in the SPV of the other entity.23 This is standard practice in the industry for the diversification of the risks. A timeline of the essential events following this is in the table below:

Table 1: Timeline of key events in SEBI v. Abhijit Rajan

|

Date |

Event description |

|

9-8-2013 |

The Board passed a resolution authorising the termination of both SHAs. (UPSI-1) |

|

22-8-2013 |

Mr Rajan sold 144 lakhs shares of GIPL. |

|

30-8-2013 |

GIPL made a disclosure to the NSE and the BSE (this is when the information became public). |

For our discussion, there is profit in dwelling upon two central issues identified by the Supreme Court in its judgment. First, whether the termination of SHAs amounted to “price-sensitive information”.24 Second, whether Mr Rajan’s trading amounted to insider trading, attracting liability under the 1992 PIT.25

A. Identification of UPSI

Regulation 2(ha)26 creates a deeming fiction where events falling under Entries (i) to (vii) will be considered price-sensitive information.27 On the first count, the Court noted that the termination of the SHAs fell squarely within the ambit of Entry (vii) of Regulation 2(ha). The entry includes “significant changes in policies, plans or operations of the company”,28 which, according to the Court, is quite broad and contemplates looking into the possibility of the information materially affecting the scrip prices.29 This, in turn, extends to factoring in the “profit motive” of the wrongdoer. The Court thus found a distinction between the first six entries and the last because it is broad. Distinguishing these entries exposes a logical fallacy of argumentation (also known as petitio principii or circular argument), where the premise logically depends on the argument’s conclusion.30

In law, the word “deem” establishes a legal fiction either positively by “deeming” something to be something it is not or negatively by “deeming” something not to be something which it is.31 Thus, the entries set out in Regulation 2(ha)32, by default, result in price-sensitive information regardless of what they are. However, by injecting the “profit motive” into the Entry (vii), the Court has rendered it redundant since it requires further examination.

B. Emphasis on “profit motive”

On the second count, it is conventional wisdom that any insider would wait for the information to become public before taking any action if the nature of the UPSI is positive. Here, Mr Rajan encashed his securities while the information was still unpublished.33 Therefore, his action was diametrically opposite to the anticipated share price movement. The Supreme Court observed that Mr Rajan executed the trades out of necessity by contributing to the corporate debt restructuring (CDR) package.34 If he had not paid towards the package, the parent company of GIPL would have had to file for bankruptcy. This act led the Court to conclude that he did not have the motive to make gains since the UPSI was positive, and any wrongdoer would have waited for the information to become public before selling the shares to make a profit.35

The Court clarified that it is the “profit motive” and not the actual gain that is indispensable to constitute an offence of insider trading.36 However, introducing such a standard makes a rigorous fact-based examination essential, eventually introducing subjectivity. It is paradoxical for the Court to introduce an element of subjectivity when it outright rejected applying the de minimus doctrine (by which courts refuse to consider trifling matters) solely on the ground that it will inject subjectivity into insider trading provisions.37

The letter and spirit of Indian law

Despite the ruling in Abhijit Rajan38, it is vital to note that the spirit of Indian law differs from American and British law. In the United States of America (USA), insider trading is pigeonholed as a type of securities fraud, governed by the general law of fraud.39 Therefore, as seen in Dirks v. Securities and Exchange40 and United States of America v. Newman41, mens rea, motive, and intention to make a profit are relevant and must be established before an insider trading charge can be made.

Likewise, in the United Kingdom (UK), Section 52 of the Criminal Justice Act, 199342 prohibits insider trading. Section 53 recognises three defences for individuals accused of insider trading — (a) it was not expected at the time of dealing that the transaction would result in a profit; (b) the accused was under the impression that the information is within the public domain; and (c) that transaction would have been undertaken even without access to the sensitive information.43 As the offence entails criminal liability, the requirement of mens rea is indispensable to constitute an insider trading offence in the UK.

Thus, as noted in the SEBI order against DSQ Holdings Ltd.,44 we cannot draw parallels between Rule 10(b-5) of the Securities Exchange Act, 1934 (USA) and the SEBI (PIT) Regulations. The UK’s Criminal Justice Act, 1993 provisions also stand on a different footing than the SEBI Act and Regulations. For this reason, we cannot import either into the Indian insider trading legislation. Even the erstwhile Section 195 of the Companies Act, 201345, which penalised any director or key managerial personnel for insider trading with either or both of imprisonment and fine, did not make “profit motive” or mens rea a necessary criterion to attract liability.46

At first blush, the “necessity” argument advanced by Mr Rajan sounds convincing, but can we introduce an element of motive in an offence which is not designed to take it into account? The 2006 case of SEBI v. Shriram Mutual Fund (Shriram)47 where the Supreme Court impliedly overruled the mens rea requirement comes in handy to answer this question. This case involved a question as to whether imposing a penalty is a sine qua non after it has been proven beyond a reasonable doubt that the mutual fund has broken the provisions of the certificate of registration and the statutory regulations i.e. SEBI (Mutual Funds) Regulations, 199648. Although the case did not involve insider trading, and the Court’s observations were primarily concerning mens rea, which already stands distinguished with the “profit motive” standard culled out in Abhijit Rajan49, it provides some compelling arguments concerning reading the requirement of “motive” into the provisions listed under Chapter VI-A of the SEBI Act, 199250.

Interpreting the statutory scheme of the SEBI Act, 1992,51 the Supreme Court held that Sections 15-A to 15-HB52 are in the form of mandatory provisions imposing penalties in default of the SEBI Act and Regulations provisions.53 Put simply, the breach of a civil obligation which attracts a penalty under the provisions of an Act would immediately attract the levy of penalty regardless of whether the violation was committed with a guilty intention or not.54 The Court’s observations are squarely applicable to interpreting Abhijit Rajan55 since the penalty for insider trading is listed under Section 15-G of Chapter VI-A of the SEBI Act, 1992.56 Without any stretch, we can reasonably extend the observation of the Supreme Court in the case mentioned above regarding guilty intention to the “profit motive” requirement, which will rule out the possibility of introducing the “profit motive” standard in insider trading law. Abhijit Rajan57 becomes more so curious when one considers the fact that it was delivered by a Division Bench of the Supreme Court and, therefore, could not impliedly overrule the observations of the Division Bench regarding Chapter VI-A of the SEBI Act in Shriram58.

One can notice a disparity in the language of the text of Section 15-G of the SEBI Act, 1992, which uses the term “on the basis” of UPSI.59 Meanwhile, Section 12-A uses the term “while in possession” of UPSI.60 The Committee on Fair Market Conduct recommended that Section 15-G be aligned with Section 12-A instead of vice versa.61 This recommendation clarifies that the regulator wants to stick with the “possession” standard rather than the “use” standard, which could incorporate getting into the why of the trades. Further, India subscribes to the “parity of information” approach, where possession is more important than the insider’s intent to violate the law.62 Although the approach accommodates certain exceptions, the “profit motive” requirement has an effect of broader erosion of this theory.

All in all, adding any extra requirements to the provisions of Chapter VI-A is clearly against the letter and spirit of the law. It defeats the entire goal of the chapter, which provides SEBI with the necessary teeth to ensure rigorous compliance with the Act and the Regulations.63 Besides, injecting the subjective element of profit motive might affect the deterrent effect of the law, as individuals may argue their way out of charges by presenting alternative motives for their trades.

One may, of course, argue for the relevance of mens rea under Section 24 of the SEBI Act.64 However, initiating criminal proceedings remains a matter of SEBI’s discretion and has thus been done just 11 times in the 24 years from 1992 to 2016, including in the previously cited DSQ Holdings Ltd.65 The sparing use of criminal remedies is possibly attributed to the high burden of proof beyond reasonable doubt and therefore, have not had the desired effect.

The ramifications of Abhijit Rajan

While Abhijit Rajan66 has been regarded as a watershed moment in the history of securities law, there is more than one incongruity in the reasoning advanced by the Supreme Court in reaching this conclusion. Before 2002, insiders were prohibited from dealing in securities “on the basis” of UPSI. The 2002 Amendment67 to the 1992 PIT introduced the “possession standard” to the regulations. Then on, mere possession of UPSI at the time of trading would trigger contravention.68 This continued even under the 2015 PIT, which ex facie neither requires proof of use nor any motive to commit insider trading.69 Broadly, the present ruling has the effect of diluting this provision and rendering it redundant.

What is required for an offence to be committed is that the insider was in possession of UPSI at the time of trading.70 The legislative note to Regulation 4(1) of the 2015 PIT further clarifies that “the reasons for which he trades or the purposes to which he applies the proceeds of the transactions are not intended to be relevant for determining whether a person has violated the regulation”.71 Effectively, whether such a trade leads to a profit or loss is irrelevant to the offence of insider trading.

As the N.K. Sodhi Committee observed, legislative notes are integral and operative parts of the regulations. They aim to inform society what role the regulatory system expects the provision of the regulation to perform and help in their interpretation.72 In light of this, the extant regulations do not contemplate this standard created by the Supreme Court. Strictly speaking, if one were to look at the present case against the text of the 2015 PIT, Rajan’s contribution to the CDR package would be irrelevant in determining his guilt since the reasons he trades are not intended to be considered.

An insider may escape the clutches of penalisation by proving his innocence, including by applying the defences set out in Regulation 4. Exceptions to the deeming fiction (i.e. trading while possessing UPSI shall be deemed motivated by UPSI) created under Regulation 4 include inter se transfer, transactions through block deal mechanism, transactions pursuant to ESOPs, etcetera.73 When the regulations already recognise exceptions, it makes little sense to introduce a vaguer standard, giving ample scope to a wrongdoer to escape liability, as exhibited in the following three scenarios:

A. Positive UPSI

Consider, for one, that a person, Jane Doe, receives and is in possession of information about significant changes in policies, plans, or operations of a company, ABC Ltd., which is likely to impact its stock price positively when published. She thus buys shares before the information is in the public domain to encash the benefit once the prices rise. Contrary to her belief, the prices fall, and she makes no actual gain, which is common following earnings surprises.74 Despite the Supreme Court clarifying the dispensability of actual gain, she now has the trump card of lack of a profit motive, a factual assessment by which Jane and many others can escape liability.

B. Negative UPSI

In the second scenario, Jane possesses a similar UPSI, but that is likely to impact the stock price of ABC Ltd. when published. Like Abhijit Rajan75, the prices rose after the UPSI came into public knowledge (reminiscent of Redditors short-squeezing GameStop stock that eventually led Melvin Capital to bankruptcy76). At the same time, Jane has already sold her shares to stop losses. Instead of the act attracting a penalty for trading while in possession of UPSI, there is now a subjective assessment of her motive, contrary to the letter and spirit of Indian securities law.

C. Mixed motives

Further, the third pertinent question involves mixed motives. Consider that Jane buys stock in ABC Ltd. after a lawyer, aware of its confidential merger and acquisition plans, tips her about the transaction. Now, her actions were not motivated only by these tips. She conducted “fundamental” research supporting the stock’s value and concluded it was undervalued. She also learnt about rumours that hinted at the transactions her lawyer friend had introduced her to.77 Suddenly, things start becoming grey since her act of trading in the securities was motivated by her analysis and the tip obtained from her friend. Should the courts use the “but for” standard (that an act is the cause of an outcome if it would not have occurred without that act) to identify the actual cause of the trade? Or should they still make her liable even if other needs and knowledge overdetermined the trade (on the premise that every slightest illegal reason will tarnish the action)?78 These are novel questions that Indian jurisprudence has yet to answer.

Envisaging a solution

Trading in securities is akin to playing cricket. However, unlike the sport, one needs to learn who they are playing as they are dealt multiple deliveries from different directions of the pitch. It is not unreasonable for the Supreme Court to have estimated in Abhijit Rajan what constitutes normal human conduct.79 Nevertheless, at best, human expectations of how the markets will respond to information are a hope — a virtue destined never to leave humankind. As C.P. Chandrasekhar puts it, “predicting stock market trends is indeed a hazardous occupation”.80 There is no guarantee that such expectations may manifest favourably for the investor, evidenced by the irrational pricing in Q3FY24, barely reflective of the underlying fundamental value of the respective companies.81

We live in such times that, irrespective of the earnings per share targets (EPS) and the return on equity (RoE), investor psychology and behavioural biases fuel stock prices to the moon. Against this complex background, the most vulnerable stakeholder is the retail investor. So long as normative aspects of motive are attributed to insider trading, the same retail investor stands to lose. Therefore, one may consider the practices followed by other mature jurisdictions with a robust insider trading regime to envisage a solution. In Singapore, for instance, insider trading is punishable under the Securities and Futures Act, 2001.82 The provision makes it amply clear that “it is not necessary for the prosecution or claimant to prove that the accused person or defendant intended to use the information referred to in Section 218(1)(a) or Section (1-A)(a) or Section 219(1)(a) in contravention of Section 218 or Section 219, as the case may be”.83 It can be seen that the Singaporean legislation outrightly shuns the relevance of motive while pinning down an offence of insider trading.

The authors opine that the courts should stay within the plain text of the 1992 PIT and the 2015 PIT or change their scope entirely, especially when the statutes are plain and unambiguous.84 Per the rule of interpretation, adding words into statutes must be avoided unless the section is meaningless or doubtful.85 For instance, in British India General Insurance Co. Ltd. v. Itbar Singh86, the Supreme Court refused to add words to the erstwhile Motor Vehicles Act, 1939, as Section 96(2)87 was exhaustive of the defences open to an insurer.88 The Supreme Court has also quoted and approved that the statute’s language should be read as is in Harbhajan Singh v. Press Council of India89 and Sakshi v. Union of India.90 As observed in Inco Europe Ltd. v. First Choice Distribution91, while discharging the interpretative function, the Court can add words only to correct obvious drafting errors, which are not apparent in the 1992 PIT and the 2015 PIT.

Further, we can understand the regulator’s intent from a consultation paper released by SEBI in 2008 on the introduction of “short swing profit” regulation in India.92 An essential feature of the proposed rule was that it just takes the existence of an insider and the execution of buy and sell trades within a six-month time-frame to trigger the surrender requirement. Intent or motive was not considered a prerequisite in this proposed regulation. Considering the broad scope that the “profit motive” standard offers wrongdoers, the easiest solution to ensure compliance is to hit the reset button. In the absence of an explicit defence recognised under the 1992 and the 2015 PIT, “profit motive” (or lack of it) may be a relevant factor in assessing the amount of penalty in a particular case of insider trading, rather than an additional limb or requirement for sustaining the charge itself.

Conclusion

Considering this discussion, it is imperative to get some clarity before it becomes too late. In fact, in line with Abhijit Rajan93, an (Securities Appellate Tribunal) SAT order dated 2-2-202394, which dealt with violations under the 1992 PIT, has already been added to the list of rulings which emphasised the relevance of establishing an insider’s motive to hold him liable for an offence of insider trading.

It will be interesting to see if Abhijit Rajan95 becomes the final word on the matter or if the security market watchdog contemplates a review of the decision. With many terming its move as regulatory overreach and since more than 30 days have passed since the judgment, the latter seems unlikely, as SEBI has thrown in the towel. Following stare decisis, any future review petition will also be subject to a highly rigorous process.

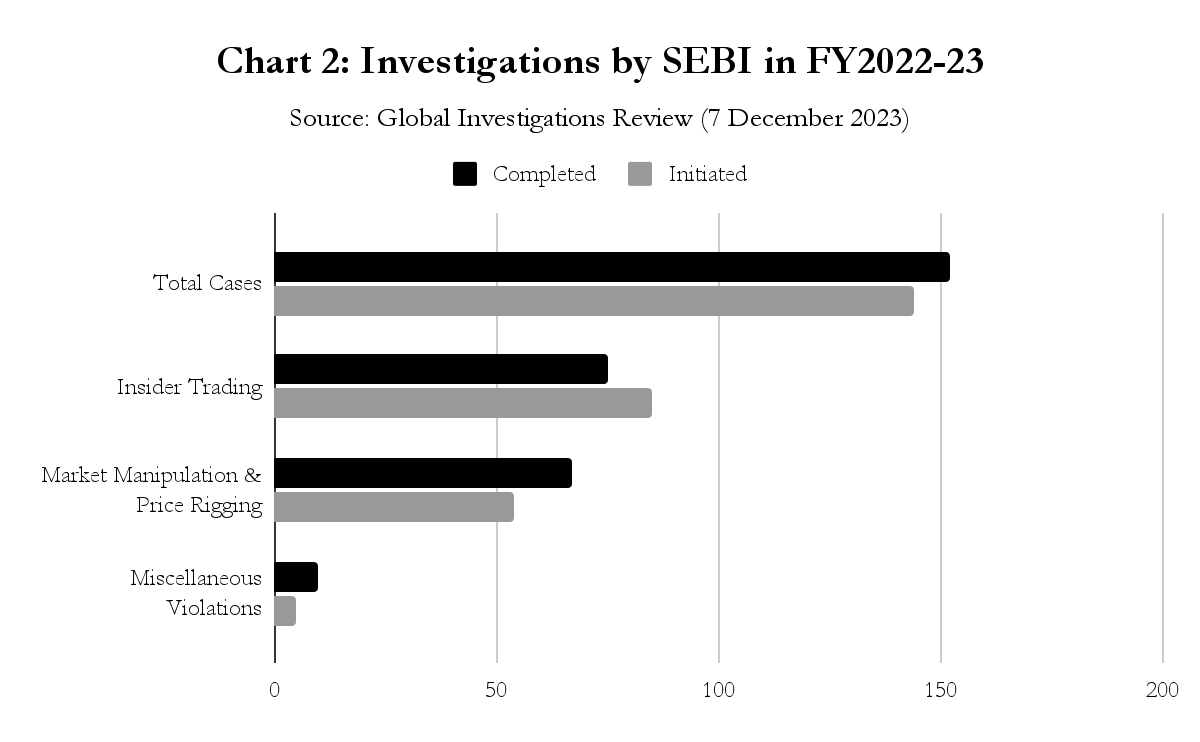

In FY 2022-2023 alone, 85 (59%) of the 144 investigations initiated by SEBI involved insider trading and of the 152 completed, 75 (49.3%) involved insider trading cases.96 While a higher standard of proof shall be an indispensable requirement before holding a person liable for insider trading, in the greater scheme of things, the Supreme Court’s act of introducing the “profit motive” requirement paves the way for several wrongdoers to disregard the law with impunity and then plead that they had no “commercial motivation” to avoid liability and punishment. To conclude with a poignant metaphor, “it is akin to someone robbing a bank with the intention of donating the money to charity. The noble end would not immunise the ignoble means of achieving that end from legal punishment”.

†Fifth year student, pursuing BBA LLB (Hons.) at Gujarat National Law University. Author can be reached at <aniketpanchal1120@gmail.com>.

††Fifth year student, pursuing BA LLB (Hons.) at Gujarat National Law University. Author can be reached at <sidharthpai26@gmail.com>.

1. Tobin Hart, “Chapter 2: The Currency of Information” in Counterpoints (2009) 162 From Information to Transformation: Education for the Evolution of Consciousness: Revised Edition 15-31 <https://www.jstor.org/stable/42977396?seq=1> accessed 09-05-2024.

2. “Information for the Public: Markets with Asymmetric Information” (The Nobel Prize, 2001) <https://www.nobelprize.org/prizes/economic-sciences/2001/popular-information/> Last accessed on 09-05-2024.

3. Grant McCool, “Rajat Gupta gets Sentencing Support from Gates, Annan” (www.reuters.com, 13-10-2012).

4. SEBI (Prohibition of Insider Trading) Regulations, 2015.

5. N.K. Sodhi Committee, Report to Review the SEBI (Prohibition of Insider Trading) Regulations, 1992, (December 2013).

6. N.K. Sodhi Committee, Report to Review the SEBI (Prohibition of Insider Trading) Regulations, 1992, (December 2013), para 1.

7. International Organisation of Securities Commission, Objectives and Principles of Securities Regulations, 2003.

8. Securities and Exchange Board of India Act, 1992.

9. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992, Reg. 3.

10. Armaan Patkar, Insider Trading Law and Practice (Eastern Book Company, Lucknow, 2019).

11. Armaan Patkar, Insider Trading Law and Practice (Eastern Book Company, Lucknow, 2019).

15. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992, Reg. 3.

16. Rakesh Agrawal v. SEBI, 2003 SCC OnLine SAT 38, para 173.

17. Rakesh Agrawal v. SEBI, 2003 SCC OnLine SAT 38, para 173.

18. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

19. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992.

21. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 3

22. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 3.

23. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 3.

24. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, paras 3 and 4.

25. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 3; Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992.

26. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992, Regn. 2(ha).

27. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 25.

28. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992, Regn. 2(ha).

29. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 26.

30. Umakanth Varottil, “Supreme Court on Motive as a Precondition for Insider Trading” (indiacorplaw.in, 26-9-2022).

31. G.C. Thornton, Legislative Drafting (2nd Edn., Butterworths 1979) pp. 83-84.

32. Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992, Regn. 2(ha).

33. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 3.

34. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

35. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 33-34

36. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 30.

37. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 38.

38. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

39. DSQ Holdings Ltd., In re (Unfair Trade Practice), 2004 SCC OnLine SEBI 362.

40. 1983 SCC OnLine US SC 165 : 77 L Ed 2d 911 : 463 US 646 (1983).

41. 773 F 3d 438 (2d Cir 2014).

42. Criminal Justice Act, 1993, S. 52.

43. Criminal Justice Act, 1993, S. 53.

44. DSQ Holdings Ltd., In re (Unfair Trade Practice), 2004 SCC OnLine SEBI 362..

45. Companies Act, 2013, S. 195.

46. Suneeth Katarki and Namita Viswanath, “Mens Rea in Insider Trading — A Sine Qua Non” (mondaq.com, 3-6-2015).

48. SEBI (Mutual Funds) Regulations, 1996.

49. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 43

50. Securities and Exchange Board of India Act, 1992, Ch. VI-A.

51. Securities and Exchange Board of India Act, 1992, S. 15-G.

52. Securities and Exchange Board of India Act, 1992, Ss.15-A to 15-HB.

53. SEBI v. Shriram Mutual Fund, (2006) 5 SCC 361, para 15.

54. SEBI v. Shriram Mutual Fund, (2006) 5 SCC 361, para 22.

56. Securities and Exchange Board of India Act, 1992, S. 15-G.

59. Securities and Exchange Board of India Act, 1992.

60. Securities and Exchange Board of India Act, 1992, S. 12-A.

61. Dr T.K. Vishwanathan Committee (SEBI), Report on Fair Market Conduct (8-8-2018).

62. Umakanth Varottil, “Due Diligence in Share Acquisitions: Navigating the Insider Trading Regime” (2017) 3 Journal of Business Law 237-259 (papers.ssrn.com, 13-5-2017).

63. SEBI v. Shriram Mutual Fund, (2006) 5 SCC 361, para 36.

64. Securities and Exchange Board of India Act, 1992, S. 24.

65. DSQ Holdings Ltd., In re (Unfair Trade Practice), 2004 SCC OnLine SEBI 362. See also, Armaan Patkar, Insider Trading Law and Practice (Eastern Book Company, Lucknow, 2019).

66. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

67. SEBI (Amendment) Act, 2002.

68. Alpana R. Kirloskar v. SEBI, 2023 SCC OnLine SAT 1074.

69. Armaan Patkar, Insider Trading Law and Practice (Eastern Book Company, Lucknow, 2019).

70. C.S. Bhuwneshwar Mishra, Law Relating to Insider Trading — A Comprehensive Commentary on SEBI (Prohibition of Insider Trading) Regulations 2015 (Taxmann, 2016).

71. SEBI (Prohibition of Insider Trading) Regulations, 2015, Regn. 4.

72. N.K. Sodhi Committee, Report to Review the SEBI (Prohibition of Insider Trading) Regulations, 1992, (December 2013) (N.K. Sodhi Report).

73. SEBI (Prohibition of Insider Trading) Regulations, 2015, Regn. 4.

74. James Chen, “Earnings Surprise: Overview, Examples, and Formulas” (www.investopedia.com, 10-6-2021).

75. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

76. Matthew Fox, “Melvin Capital to Shut Down One Year after GameStop Short-squeeze Caused Billions in Losses for the Hedge Fund” (www.businessinsider.in, 19-5-2022).

77. United States of America v. Teicher, 987 F 2d 112, 112 (2d Cir 1993).

78. Andrew Verstein, “Mixed Motives Insider Trading”, (2021) 106(3) Iowa Law Review 1253.

79. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241, para 38.

80. C.P. Chandrasekhar, “Is the Indian Stock Market Headed Towards a Crash?” (frontline.thehindu.com, 11-1-2024).

81. C.P. Chandrasekhar, “Is the Indian Stock Market Headed Towards a Crash?” (frontline.thehindu.com, 11-1-2024).

82. Securities and Futures Act, 2001 (Singapore).

83. Securities and Futures Act, 2001 (Singapore), Ss. 218(1)(a) & (1-A)(a) and 219(1)(a).

84. A.N. Roy v. Suresh Sham Singh, (2006) 5 SCC 745.

85. G.P. Singh, Guiding Rules in Principles of Statutory Interpretation (also including General Clauses Act, 1897 with Notes) (14th Edn., LexisNexis, 2020).

87. Motor Vehicles Act, 1939, S. 96(2).

91. (2000) 1 WLR 586 : (2000) 2 All ER 109, 115.

92. SEBI, Consultative Paper on Introduction of “Short Swing Profit” Regulations in India (sebi.gov.in, 01-1-2008).

93. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

94. Quantum Securities (P) Ltd. v. SEBI, 2023 SCC OnLine SAT 615.

95. SEBI v. Abhijit Rajan, 2022 SCC OnLine SC 1241.

96. Manjari Tyagi, Deepika Goyal, Vishnu Sumanth, & Abhiroop A Datta, “India: A Deep Dive into SEBI and Related Legislation Amid Insider Trading and Market Manipulation Investigations” (globalinvestigationsreview.com, 7-12-2023).