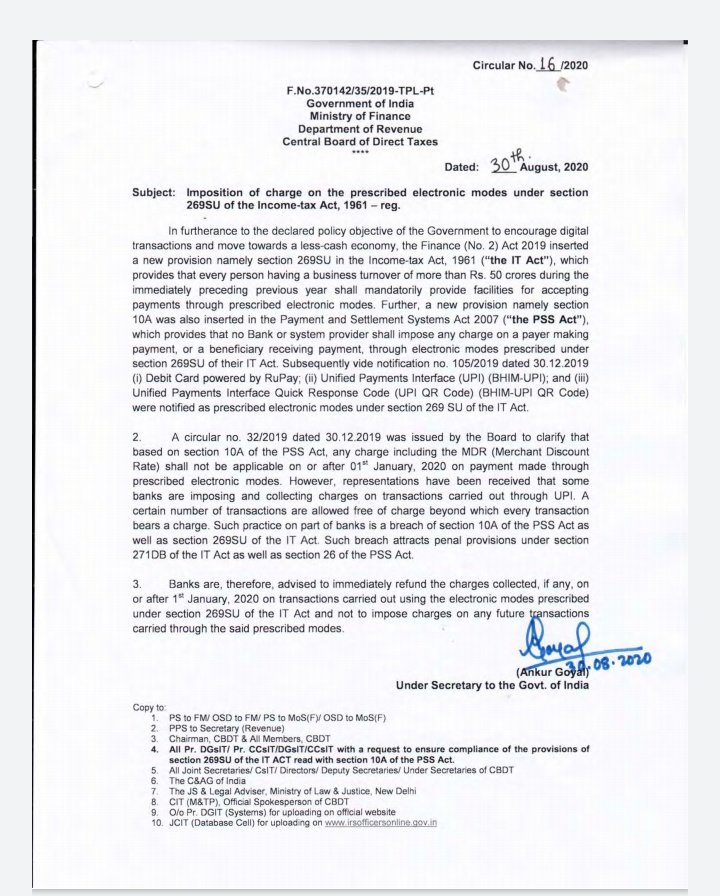

Central Board of Direct taxes notifies a clarification that the imposition of a charge on the prescribed electronic modes under Section 269 SU of the Income Tax Act.

Based on Section 10 A of the Payment and Settlement Systems Act, 2000, any charge including the Merchant Discount Rate shall not be applicable on or after 01-01-2020 on payment made through prescribed electronic modes.

However, representations have been received that some banks are imposing and collecting charges on transactions carried out through UPI. A certain number of transactions are allowed free of charge beyond which every transaction bears a charge.

The above-stated act on part of banks is a breach of Section 10 A of the PSS Act as well as Section 269SU of the IT Act. Such breach attracts penal provisions under Section 271 DB of the IT Act as well as Section 26 of the PSS Act.

Therefore, bank are advised to immediately refund the charges collected, if any, on or after 1st January, 2020 on transactions carried out using the electronic modes prescribed under Section 269 SU of the IT Act and not to impose charges on any future transactions carried through the said prescribed modes.

Following were prescribed electronic modes under Section 269 SU of the Income Tax Act:

- Debit Card powered by RuPay

- Unified Payments interface (UPI)(BHIM-UPI)

- Unified Payments Interface Quick Response Code (UPI QR Code) (BHIM-UPI QR Code)